INTRODUCTION

The first step in payroll work is to determine the gross wages or salary earned by each employee. There are several bases for computing the employee's earnings. Some workers are paid at a stated rate per hour, and their gross pay depends on the number of hours they work. This method is called the hourly rate basis. Other workers are paid an agreed amount for each week or month or other period. This arrangement is called the salary basis. Salespeople are sometimes paid on a commission basis, usually some percentage of net sales. In manufacturing, wages are sometimes based on the number of units produced. This pay system is called piece-rate basis.

Determining Hourly Employees' Gross Pay

To determine the gross pay earned by an employee on an hourly rate basis, it is necessary to know the rate of pay and the number of hours the employee has worked during the payroll period.

HOURS WORKED

There are various methods of keeping track of the hours worked by each employee. At Marcof’s Furniture, Tricia Jones, the payroll clerk, is responsible for verifying the employees’ total hours worked for the previous week. As well as she manually prepares the company’s payroll on MS Excel and gives it to Ms. Marcof for approval. Every Wednesday she collects all employees’ timesheets/cards and uses them to determine the total hours worked and prepare the payroll to be paid on the following Monday.

Many businesses use time clocks for employees, especially for those paid on an hourly basis. Each employee has a timecard and inserts it in the time clock to record the time of arrival and the time of departure.

The payroll clerk collects the cards at the end of the week, determines the hours worked by each employee, multiplies the number of hours by the proper rate, and computes the gross pay. Some timecards can be fed into a computer, which determines the hours worked and makes all earnings calculations.

Many businesses use time clocks for employees, especially for those paid on an hourly basis. Each employee has a timecard and inserts it in the time clock to record the time of arrival and the time of departure.

The payroll clerk collects the cards at the end of the week, determines the hours worked by each employee, multiplies the number of hours by the proper rate, and computes the gross pay. Some timecards can be fed into a computer, which determines the hours worked and makes all earnings calculations.

MARCOF'S EMPLOYEES #1 & #2 COMPLETED TIMESHEETS

|

|

|

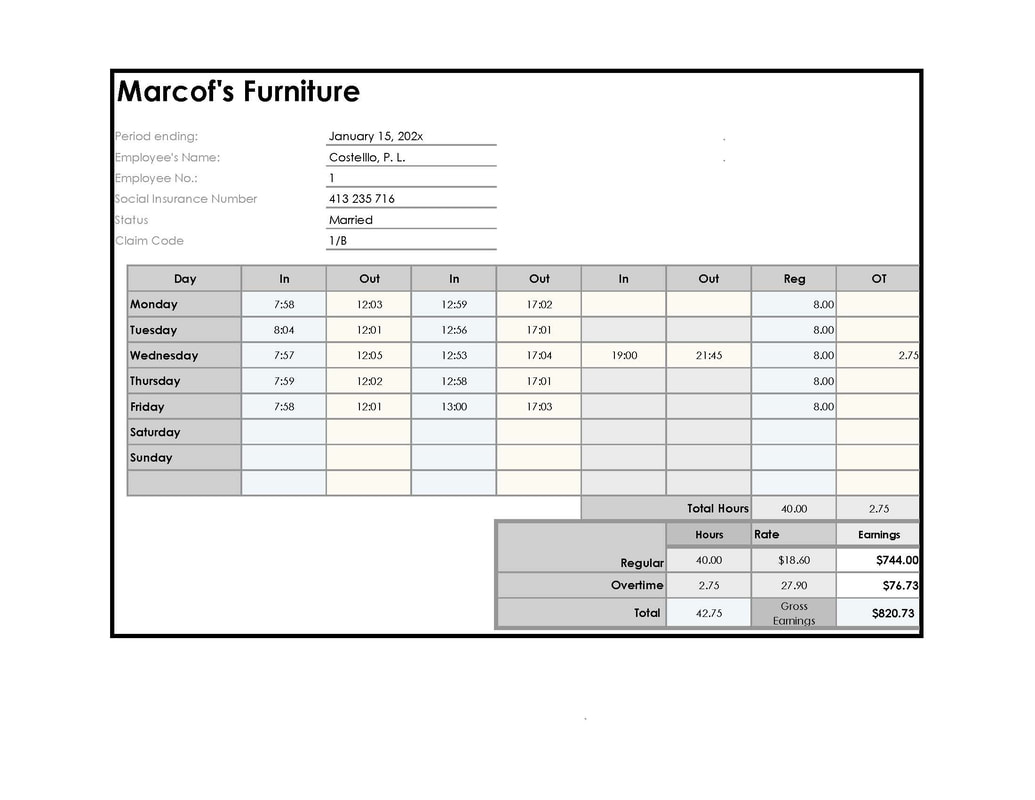

Employee #1 Completed Timecard

|

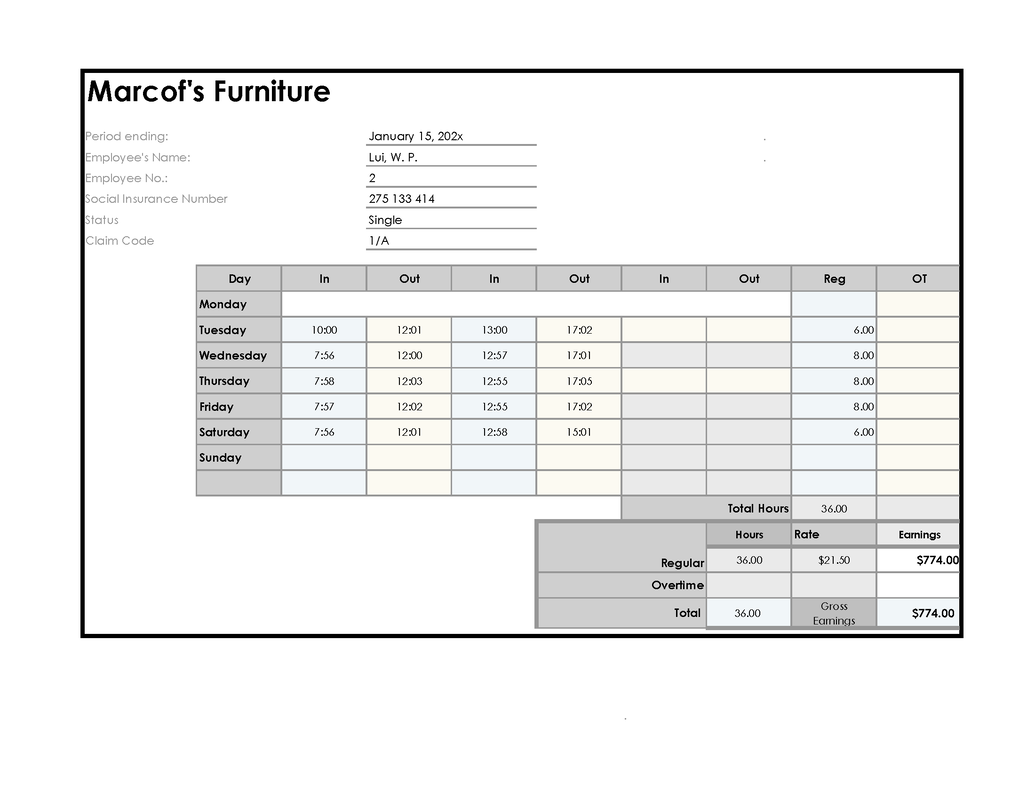

Employee #2 Completed Timecard

|

DETERMINING GROSS PAY

How to Calculation of Gross Earning

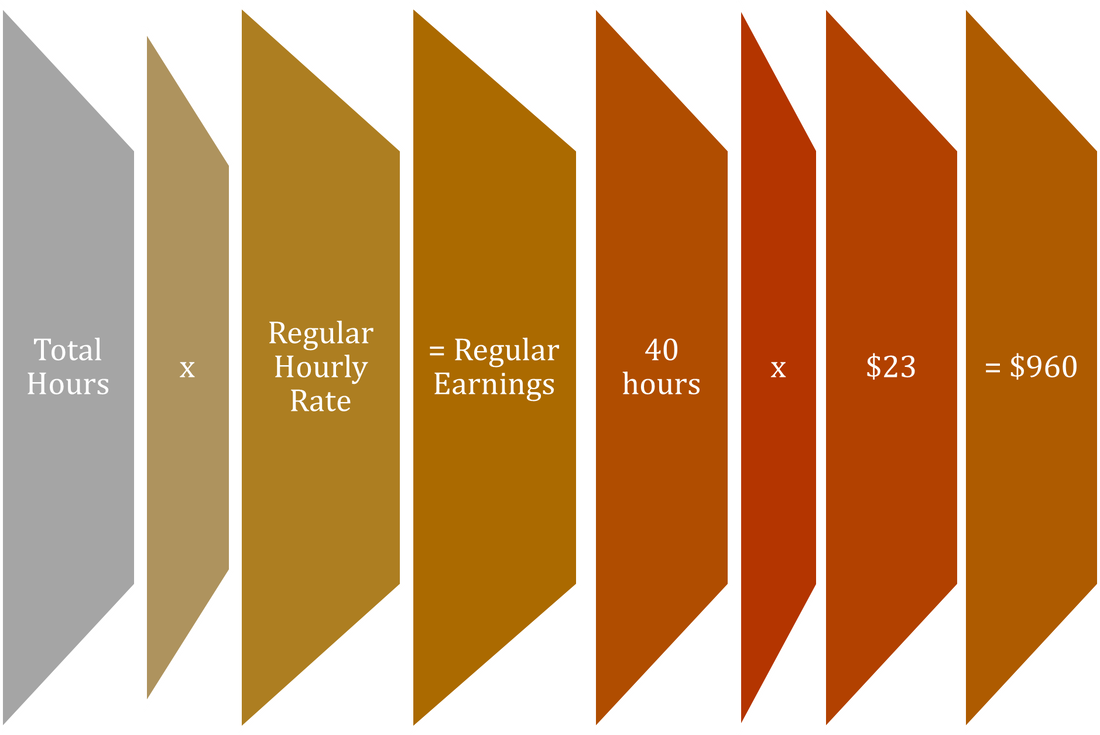

STEP 1: Calculate Regular Earnings

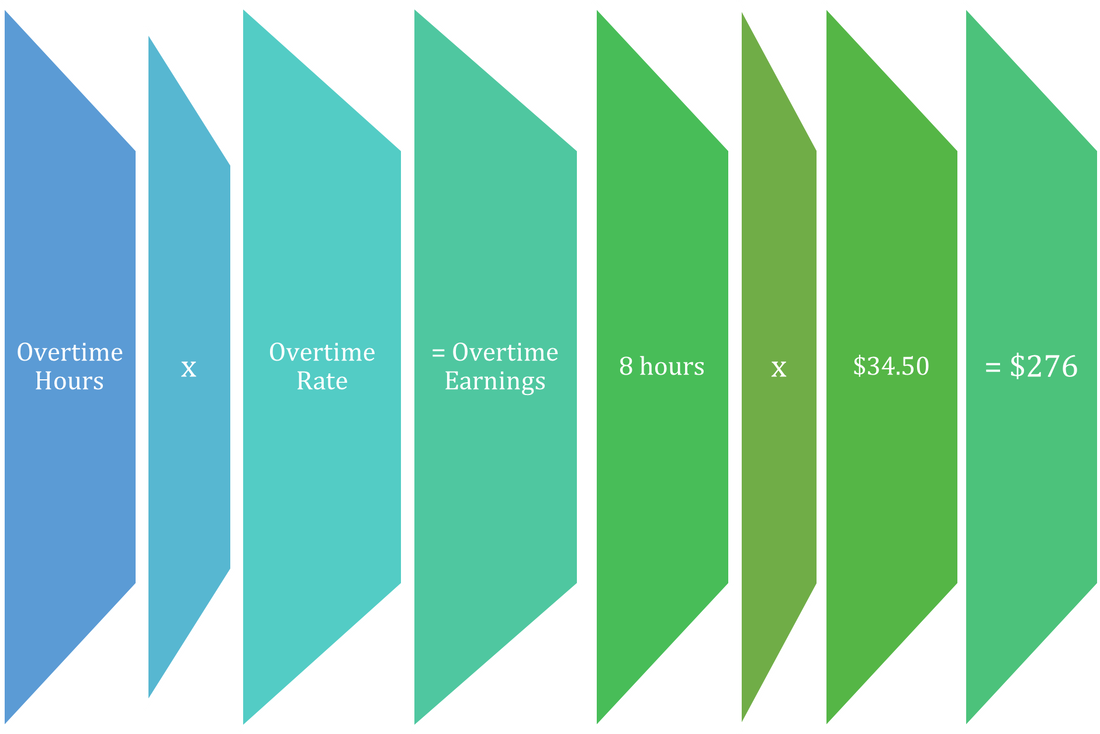

STEP 2: Calculate Overtime Pay (If Necessary)

STEP 3: Calculate Gross Earnings

Calculation of Phillipe Castello's Gross Pay

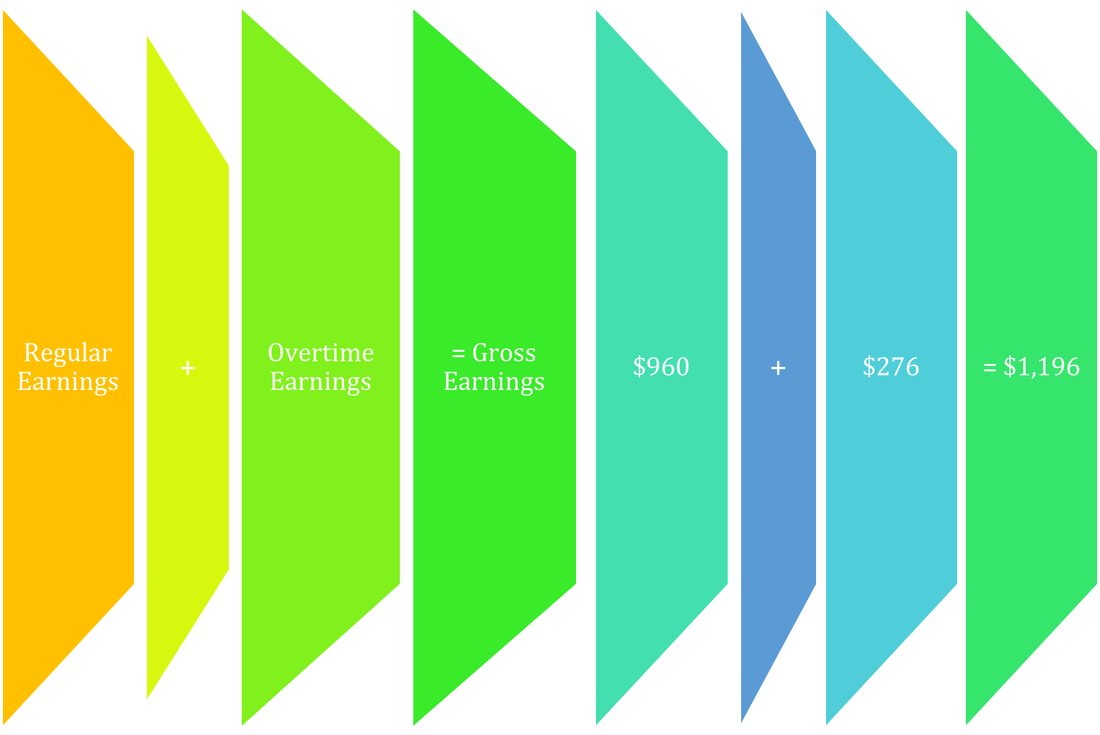

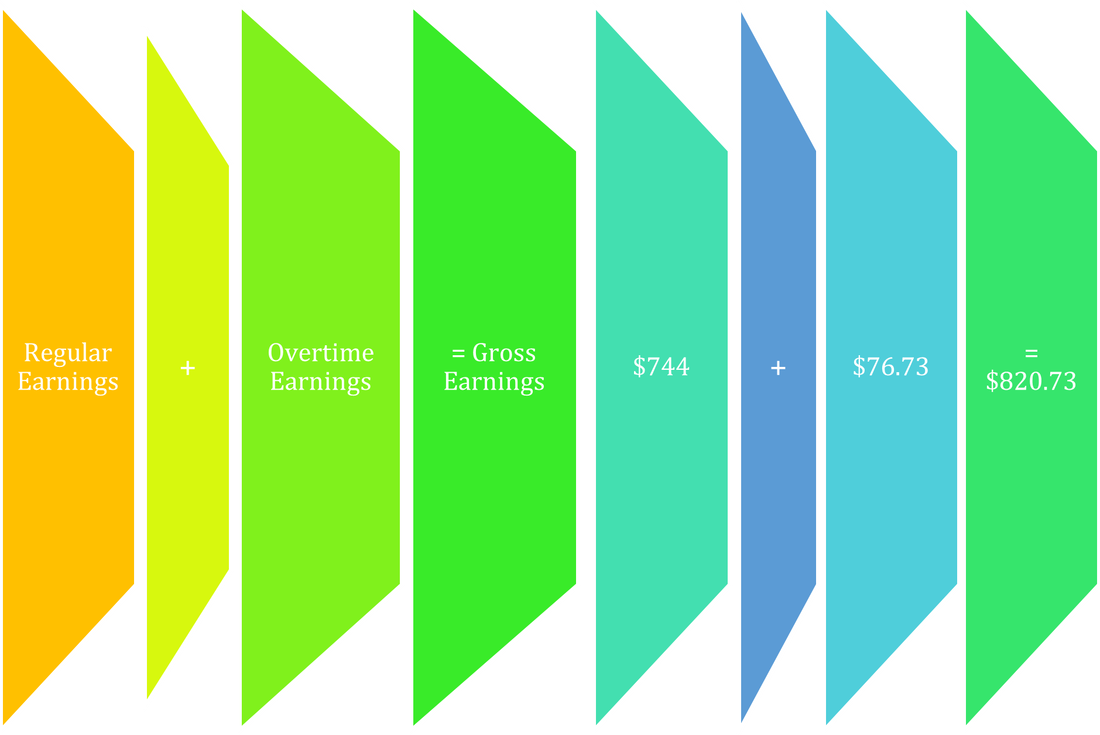

The timesheet kept at Marcof’s Furniture during the week ended January 28, 202X, shows that the first employee, Phillipe Castello, worked 42.75 hours. Two and three-quarters of these hours are overtime. Therefore, these two and three-quarters must be paid at Castello’s regular rate ($18.60) plus a premium rate ($18.60 x 1.50 = 27.90) His rate of pay is calculated by multiplying 40 hours by $18.60 per hour plus overtime two and three quarters ($27.90 x 2.75 = $76.73) for a total of $820.83. See the calculations:

Total Hours Worked = 42.75

|

Regular hours = 40

|

Regular rate $18.60

|

Overtime hours = 2.75

|

Overtime rate = $27.90

|

|

Regular Pay = 40 x 18.60 = $744.00

|

|

Overtime Pay = 2.75 x $27.90 = $76.73

|

Gross Earnings = $744.00 + $76.43

Image Gross Earnings Calculations

Phillipe Castello' s Gross Pay

The second employee, Wei Lui, worked 36 hours. His regular hourly rate is ($21.50). Therefore, his gross pay is calculated as follows:

Wei Lui's Gross Pay Calculation

|

Regular hours = 36

|

|

Hourly rate = $21.50

|

Gross Earnings = 36 X 21.50 = $774.00

Determining Salaried Employees' Gross Pay

A salary is a set amount an employee is paid for work, usually based on an annual income. Employers pay on a biweekly or semimonthly or monthly schedule and base paycheques on a fraction of the annual salary.

Therefore, a salaried employee earns a specific sum of money for each payroll period, whether it is weekly, biweekly, semi-monthly, or monthly.

For example, if an employee’s annual salary is $84,000 per year and the company pays twice a month or bi-monthly, that individual would receive receive $3,500 every paycheque before taxes and deductions. To calculate the pay for each pay period, take the annual salary of $84,000 and divide it by 24 pay periods. This equals $3,500, which is the gross pay.

Furthermore, If the company pay periods are bi-weekly the annual amount would be divided 26 equal pays, and monthly 12 equal pays. See the salary calculations for the different pay periods below. In these examples, I would be using an annual salary $92,000.

Therefore, a salaried employee earns a specific sum of money for each payroll period, whether it is weekly, biweekly, semi-monthly, or monthly.

For example, if an employee’s annual salary is $84,000 per year and the company pays twice a month or bi-monthly, that individual would receive receive $3,500 every paycheque before taxes and deductions. To calculate the pay for each pay period, take the annual salary of $84,000 and divide it by 24 pay periods. This equals $3,500, which is the gross pay.

Furthermore, If the company pay periods are bi-weekly the annual amount would be divided 26 equal pays, and monthly 12 equal pays. See the salary calculations for the different pay periods below. In these examples, I would be using an annual salary $92,000.

Calculating Salaries

Scenario 1: Annual Salary $92,000, Pay Periods Monthly

Monthly = 12 pays

Calculation of Monthly Pay

|

Annual Salary = $92, 000

|

Number of Pay Periods = 12

|

Monthly = $92, 000 / 12 =$7,666.67

Scenario 2: Annual Salary $92,000, Pay Periods Semi-monthly

Semi-monthly = 24 pays

Calculation of Semi-monthly Pay

|

Annual Salary = $92, 000

|

Number of Pay Periods = 24

|

Salary per period = $92, 000 / 24 =$3,833.33

Scenario 3: Annual Salary $92,000, Pay Periods bi-weekly

Bi-weekly = 26 pays

Calculation of Bi-weekly Pay

|

Annual Salary = $92, 000

|

Number of Pay Periods = 26

|

Salary per period = $92, 000 / 26 =$3,538.46

PAYROLL DEDUCTIONS

Canadian employers have the responsibility of paying their people. But it goes beyond just writing numbers on a cheque, and it can be very easy for new or small businesses to get lost in the complexity of payroll processing.

Businesses in Canada looking for long-term success need to manage payroll accurately from the beginning. This means compliance with the requirements of the Canada Revenue Agency (CRA), and the Ministere du Revenue du Quebec (MRQ)—in the case of Quebec--including payroll deductions. What exactly are payroll deductions? What steps do Canadian employers need to take when processing payroll? Whether they are business owners looking to ensure they are paying their employees properly, or you, as employee trying to understand where your hard-earned money is going. The examples illustrated on this website will help you effectively understand the next step in payroll process after gross earnings are determined.

Businesses in Canada looking for long-term success need to manage payroll accurately from the beginning. This means compliance with the requirements of the Canada Revenue Agency (CRA), and the Ministere du Revenue du Quebec (MRQ)—in the case of Quebec--including payroll deductions. What exactly are payroll deductions? What steps do Canadian employers need to take when processing payroll? Whether they are business owners looking to ensure they are paying their employees properly, or you, as employee trying to understand where your hard-earned money is going. The examples illustrated on this website will help you effectively understand the next step in payroll process after gross earnings are determined.

What Are Payroll Deductions?

Payroll deductions (or source deductions) are wages withheld from employees’ taxable income for the purpose of paying taxes (which are remitted, or paid to, the CRA or MRQ), garnishments (paid to creditors, including, but not limited to the CRA or MRQ), and benefits. Some deductions are voluntary, while others are mandated by the government and are required of employers, meaning an employer is liable if they fail to calculate and deduct it properly. The difference between employees’ gross income and net income is determined by these deductions. Put plainly, gross income is the wages an employee earns before deductions, and net income is the wages the employee actually takes home after deductions.

Both the business and the individual have income tax responsibilities, and the business takes care of the administration of these responsibilities throughout the year. When an individual starts a new job, they give their employer a TD1 or TP1 form, this document tells the employer a little bit about the individual’s income tax situation. The employer uses that information to calculate the employee’s income tax. At the end of the year, the employer will give the individual a T4 form, which the individual will use to file their personal income tax. The goal of a payroll calculation is to get employees as close as possible to paying/owing $0.00 in federal or provincial income taxes when they file their income tax returns.

Statutory (Mandatory) Deductions

These are the mandatory amounts that must be calculated and deducted from employees’ taxable income, then remitted to the CRA a MRQ periodically based on the type of company.

Voluntary (Optional) Deductions

Along with statutory deductions, some employers will provide benefits to their employees in the form of subsidies, resulting in additional premium amounts deducted from their wages. Examples include health insurance, Group-term life insurance retirement plans, a subsidized phone plan, gym membership and so on.

Both the business and the individual have income tax responsibilities, and the business takes care of the administration of these responsibilities throughout the year. When an individual starts a new job, they give their employer a TD1 or TP1 form, this document tells the employer a little bit about the individual’s income tax situation. The employer uses that information to calculate the employee’s income tax. At the end of the year, the employer will give the individual a T4 form, which the individual will use to file their personal income tax. The goal of a payroll calculation is to get employees as close as possible to paying/owing $0.00 in federal or provincial income taxes when they file their income tax returns.

Statutory (Mandatory) Deductions

These are the mandatory amounts that must be calculated and deducted from employees’ taxable income, then remitted to the CRA a MRQ periodically based on the type of company.

Voluntary (Optional) Deductions

Along with statutory deductions, some employers will provide benefits to their employees in the form of subsidies, resulting in additional premium amounts deducted from their wages. Examples include health insurance, Group-term life insurance retirement plans, a subsidized phone plan, gym membership and so on.

|

|

|