Items Withheld From Employees’ Wages

WHO IS AN EMPLOYEE?

The discussion of payroll accounting relates only to the earnings of those individuals classified as employees. An employee is one who is hired by the employer and who is under the control and direction of the employer. Usually, the employer provides the tools or equipment used by the employee and generally controls the employee's working hours and approach to the job. The company president, the bookkeeper, the salesclerk, and the warehouse worker are examples of employees.

In contrast to an employee, an independent contractor is paid by the company to carry out a specific task or job. The independent contractor is not under the direct supervision and control of the company. Although the independent contractor is told what needs to be done, the means of doing the job is left to the discretion of the

contractor. The accountant who performs the independent audit, the outside attorney who renders legal advice, and the computer consultant who installs a new accounting system are examples of independent contractors.

The discussion on this website and in this module relates to employees only. In dealing with independent contractors, the company is not bound by federal and provincial labour laws regulating minimum rates of pay and maximum hours of employment. Neither is the company required to withhold various employee taxes from amounts paid to independent contractors. Similarly, the company is not required to pay various payroll taxes on amounts paid to contractors.

Before examining the details of the process for computing the employee's earnings and deductions from the paycheque, let us first review some of the most important federal laws relating to employee earnings and withholding.

In contrast to an employee, an independent contractor is paid by the company to carry out a specific task or job. The independent contractor is not under the direct supervision and control of the company. Although the independent contractor is told what needs to be done, the means of doing the job is left to the discretion of the

contractor. The accountant who performs the independent audit, the outside attorney who renders legal advice, and the computer consultant who installs a new accounting system are examples of independent contractors.

The discussion on this website and in this module relates to employees only. In dealing with independent contractors, the company is not bound by federal and provincial labour laws regulating minimum rates of pay and maximum hours of employment. Neither is the company required to withhold various employee taxes from amounts paid to independent contractors. Similarly, the company is not required to pay various payroll taxes on amounts paid to contractors.

Before examining the details of the process for computing the employee's earnings and deductions from the paycheque, let us first review some of the most important federal laws relating to employee earnings and withholding.

EARNINGS AND WITHHOLDING LAWS

Since the 1930s, many federal and provincial laws that have had a crucial impact on the relationships between employers and employees have been passed. Some of these laws deal with working conditions, including hours and earnings. Others relate to taxes that must be withheld from employees' earnings and transmitted to the government by the employer. In addition, taxes are levied against the employer to provide specific employee benefits.

Let us look briefly at some of these major laws, beginning with the Labour Standards Act, which sets minimum wages and establishes a normal workweek. Later, you will learn more details on these rules and will see how the various laws relating to tax withholding and employer taxes are applied.

Let us look briefly at some of these major laws, beginning with the Labour Standards Act, which sets minimum wages and establishes a normal workweek. Later, you will learn more details on these rules and will see how the various laws relating to tax withholding and employer taxes are applied.

THE LABOUR STANDARDS ACT

The Labour Standards Act establishes a minimum hourly rate of pay and maximum hours of work per week to be performed at the regular rate of pay. As of April 1, 2023, the minimum hourly rate of pay in Quebec is $16.65. This rate is different from province to province. In addition, the standard workweek is 40 hours for most workers. This means that someone who worked 45 hours in a week did five overtime. Hours worked more than 40 in any week must be paid at an overtime rate of at least one and a half times the regular hourly rate. For more information on working hours conditions, your can read the Quebec Labor Standards In Quebec.

Many employers who are not covered by the federal or provincial laws pay time and a half for overtime because of union contracts or simply as a good business practice.

Many employers who are not covered by the federal or provincial laws pay time and a half for overtime because of union contracts or simply as a good business practice.

Employees Protected by Quebec Labour Standards Act

|

Office staff

|

Retail salespersons

|

Factory workers

|

INCOME TAX

Employers are required to withhold from the employee's earnings an estimated amount of income tax that will be payable by the employee on the earnings. The amount depends on several factors. Later on, you will learn how the employer determines how much income tax to withhold from an employee's paycheque.

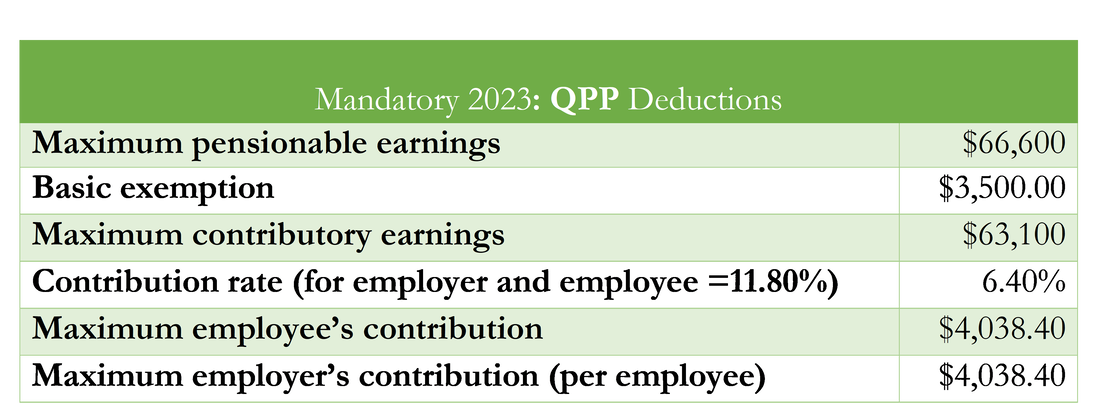

CANADA OR QUEBEC PENSION PLAN

The Canada Pension Plan (CPP) applies to all provinces, except Quebec which has its own plan-the Quebec Pension Plan (QPP)--which is similar to the CPP. The act, first passed in the 1930s, has been amended frequently. It provides certain benefits for employees and their families and levies a tax, shared equally by the employer and employee, to finance the plan.

The act provides for three major categories of benefits:

- A retirement benefit, or pension, when a worker reaches age 60.

- Benefits for the dependants of the retired worker.

- Benefits for the worker and the worker's dependants when the worker is disabled.

The rate of the CPP or QPP and the earnings base to which it applies can be changed by Parliament. For 2023, the amount to be withheld is 6.40 percent of the first $66,600 of salary or wages paid to each employee during the year, less the annual basic exemption of $3,500.

EMPLOYMENT INSURANCE

Employment Insurance (EI)

To alleviate hardships caused by interruptions in earnings through unemployment, the federal government, with the concurrence of all provincial governments, implemented an employee/employer-financed unemployment insurance plan. Under the Employment Insurance Act, 1996, compulsory employment insurance coverage was extended to all Canadian workers who are not self-employed. As of January 1,2020, over 19.8 million employees, including teachers, hospital workers, and top-level executives, were covered by the insurance plan.

The employment insurance (EI) system requires employers to pay a tax based on each employee's earnings, up to a maximum of $61,500, to finance benefits for employees who become unemployed. employers are required to deduct from their employees' wages 1.27% of insured earnings, to add a contribution of 1.4 times the amount deducted from employees' wages, and to remit both amounts to the Receiver General for Canada. The employment insurance fund from which benefits are paid is jointly financed by employees and their employers.

The employment insurance (EI) system requires employers to pay a tax based on each employee's earnings, up to a maximum of $61,500, to finance benefits for employees who become unemployed. employers are required to deduct from their employees' wages 1.27% of insured earnings, to add a contribution of 1.4 times the amount deducted from employees' wages, and to remit both amounts to the Receiver General for Canada. The employment insurance fund from which benefits are paid is jointly financed by employees and their employers.

The system is summarized as follows: insured earnings, in most instances, refer to gross earnings. An employee may receive taxable benefits or allowances that would be included in gross earnings but would not be considered insurable earnings. However, in this text, gross earnings will be insurable earnings.

The Employment Insurance Act also requires that an employer complete a "Record of Employment" because of termination of employment, illness, injury, or pregnancy and keep a record for each employee that shows among other things wages subject to employment insurance and taxes withheld.

The Employment Insurance Act also requires that an employer complete a "Record of Employment" because of termination of employment, illness, injury, or pregnancy and keep a record for each employee that shows among other things wages subject to employment insurance and taxes withheld.

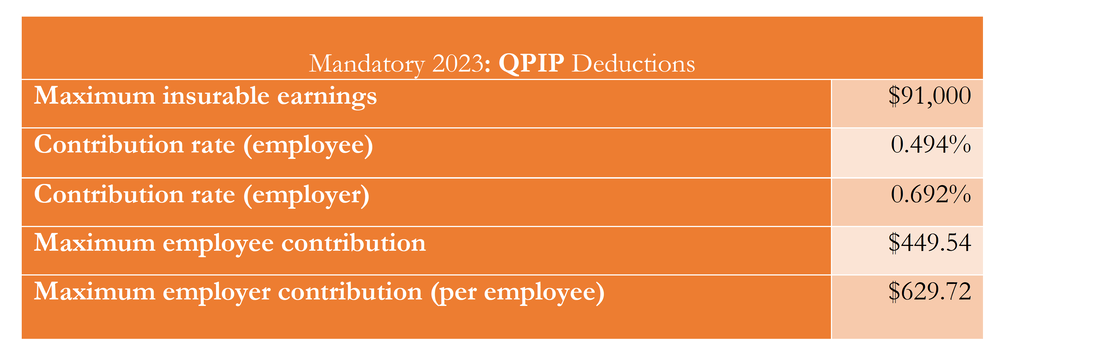

QUEBEC PARENTAL INSURANCE PLAN

The province of Quebec manages the maternity, parental, and adoption benefits for residents of Quebec under the Quebec Parental Insurance Plan (QPIP). QPIP replaces similar benefits that Quebec residents previously received under the Employment Insurance Act. Because of this, all employers who have employees working in Quebec, regardless of the employee’s province or territory of residence, have to deduct a reduced employment insurance (EI) premium using a reduced EI premium rate as well as QPIP premiums.

QPIP premiums must be paid regardless of the employee's age to a maximum of $91,000 insurable earning for 2023; the employee's place of residence (in general) and whether or not the employee receives benefits under the plan.

QPIP premiums must be paid regardless of the employee's age to a maximum of $91,000 insurable earning for 2023; the employee's place of residence (in general) and whether or not the employee receives benefits under the plan.

OTHER PAYROLL DEDUCTIONS

In some cases, employees ask to have amounts deducted from their earnings and deposited in a bank or a company credit union, or accumulated and used to buy Canada savings bonds, shares of stock, or other investments. The employee signs an authorization for such deductions and may change this authorization or terminate it at any time.

Employees who have received advances from their employers or who have bought merchandise from the firm often repay such debts through payroll deductions. When employees belong to a union, the contract between the employer and the union may specify that union dues be deducted from employee wages.

These and other possible payroll deductions increase payroll record-keeping work but do not involve any new principles or procedures. They are handled in the same way as the required deductions for Quebec Pension, Plan, employment insurance, and income taxes.

Employees may individually authorize additional deductions such as:

Employees who have received advances from their employers or who have bought merchandise from the firm often repay such debts through payroll deductions. When employees belong to a union, the contract between the employer and the union may specify that union dues be deducted from employee wages.

These and other possible payroll deductions increase payroll record-keeping work but do not involve any new principles or procedures. They are handled in the same way as the required deductions for Quebec Pension, Plan, employment insurance, and income taxes.

Employees may individually authorize additional deductions such as:

- Deductions to accumulate funds for the purchase of Canada Savings Bonds.

- Deductions to pay health, accident, hospital, or life insurance premiums.

- Deductions to repay loans from the employer or the employees' credit union.

- Deductions to pay for merchandise purchased from the company.

- Deductions for donations to charitable organizations such as the United Way

WAGES, HOURS, AND UNION CONTRACTS

All provinces have laws establishing maximum hours of work and minimum pay rates. And, while the details vary with each province, generally employers are required to pay an employee for hours worked in excess of 40 in anyone week at the employee's regular pay rate plus an overtime premium of at least one-half of his or her regular rate.

In addition, employers commonly operate under contracts with their employees' union that provide even better terms. In addition to specifying working hours and wage rates, union contracts often provide that the employer shall deduct dues from the wages of each employee and remit the amounts deducted to the union.

In addition, employers commonly operate under contracts with their employees' union that provide even better terms. In addition to specifying working hours and wage rates, union contracts often provide that the employer shall deduct dues from the wages of each employee and remit the amounts deducted to the union.

WITHHOLDING NOT REQUIRED BY LAW

Many kinds of deductions not required by law are made by agreement between the employee and the employer. For example, a specified deduction from the earnings of an employee may be made at the end of each payroll period for group life insurance or group medical insurance covering the employee's family.

Company retirement plans may be financed entirely by the employer or by the employer and employee jointly. In the latter case, employee contributions to the retirement plan are usually based on the wages or salary earned and are customarily deducted from earnings each payroll period.

Company retirement plans may be financed entirely by the employer or by the employer and employee jointly. In the latter case, employee contributions to the retirement plan are usually based on the wages or salary earned and are customarily deducted from earnings each payroll period.

THE EMPLOYER'S PAYROLL COSTS

Employers must also pay taxes on their employee's earnings. Federal taxes are levied for all Canadian or Quebec pension plans, employment insurance benefits. In addition, Quebec employers must remit their portion of the Quebec parental insurance plan (QPIP), as well as their contribution to the Quebec Health Service Fund (QHSF). Furthermore, each province requires employers to carry workers' compensation insurance.

CANADA OR QUEBEC PENSION PLAN

Under the Canada or Quebec Pension Plan rules, the employer is required to pay an amount equal to the Canada or Quebec Pension Plan tax withheld from the employee's base earnings. The employer's share of tax is remitted to the federal and provincial governments and along with the amounts withheld from the employee's paycheque. Remember that the QPP tax is 6.40 percent of the first $66,600 of gross earnings paid to each employee during the year, less the annual basic exemption of $3,500.

EMPLOYMENT INSURANCE

The employment insurance (EI) system requires employers to pay a tax based on each employee's earnings, up to a maximum of $61,500, to finance benefits for employees who become unemployed. The rate for the employment insurance premium is 1.27 percent of the employee's gross wage, The employer must pay 1.4 times the amount that the employee contributes.

QUEBEC PARENTAL INSURANCE PLAN

Under the Quebec Parental Insurance Plan employers both employers and employees must contribute to the Québec parental insurance plan (QPIP) in order to provide for the payment of benefits to employees who take unpaid maternity, paternity, adoption or parental leave. The maximum insurable earnings considered when calculating benefits are $91,000 in 2023 and the employer’s contribution rate is .692%

QUEBEC HEALTH AND SERVICE FUND

Quebec employers must contribute to the Quebec health services fund corresponding to the total salaries or wages subject to the contribution that they pay to their employees in the year multiplied by the applicable contribution rate. The rate is based on your total payroll for the year and their sector of activity.

Rates (%) for all employers other than public sector employers and employers whose total payroll is more than 50% attributable to activities in the primary and manufacturing sectors. The present rate is 1.65 percent for salaries less than one million dollars.

Rates (%) for all employers other than public sector employers and employers whose total payroll is more than 50% attributable to activities in the primary and manufacturing sectors. The present rate is 1.65 percent for salaries less than one million dollars.

WORKERS' COMPENSATION INSURANCE

Employers frequently carry workers' compensation insurance to protect employees against losses from job-related injuries or sickness. Some provinces have laws that mandate workers' compensation insurance. Under the workers' compensation program, employers pay for insurance that will reimburse employees for losses suffered from job-related injuries or compensate their families if death occurs in the course of employment, Benefits are paid directly to the injured workers or to their survivors.

In Quebec workers' compensation insurance administered the Commission des normes, de l'équité, de la santé ET de la sécurité du travail (CNESST).

In Quebec workers' compensation insurance administered the Commission des normes, de l'équité, de la santé ET de la sécurité du travail (CNESST).

EMPLOYEE RECORDS REQUIRED BY LAW

Laws related to wages, hours, withholdings, and employer payroll taxes require that certain records be maintained for each employee. The most important records required are:

- The name, address, social insurance number, and date of birth of each employee.

- Hours worked each day and week, wages paid at the regular rate, and overtime premium wages; certain exceptions exist for employees paid on a salary basis.

- Cumulative taxable wages paid throughout the year.

- Amount of income tax, Canada or Quebec pension plan contributions, and employment insurance premiums withheld from each employee's earnings for each pay period

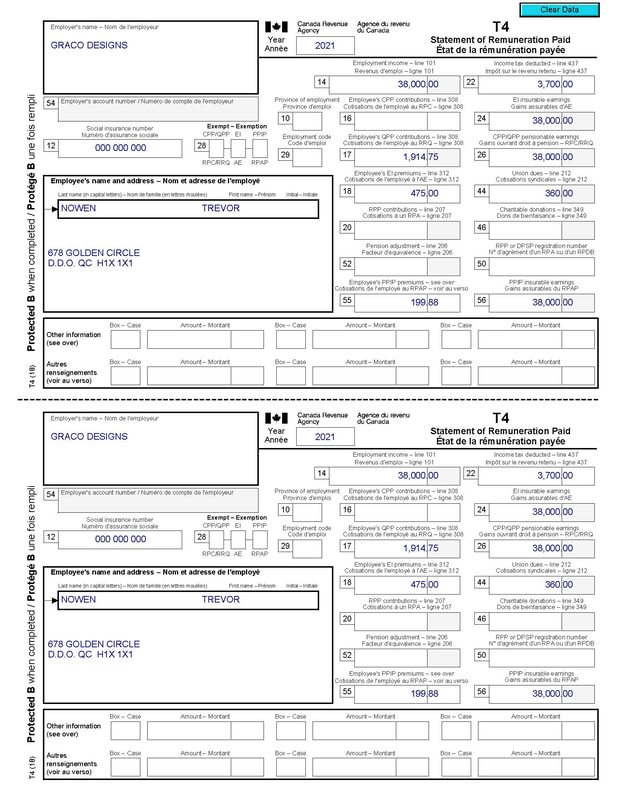

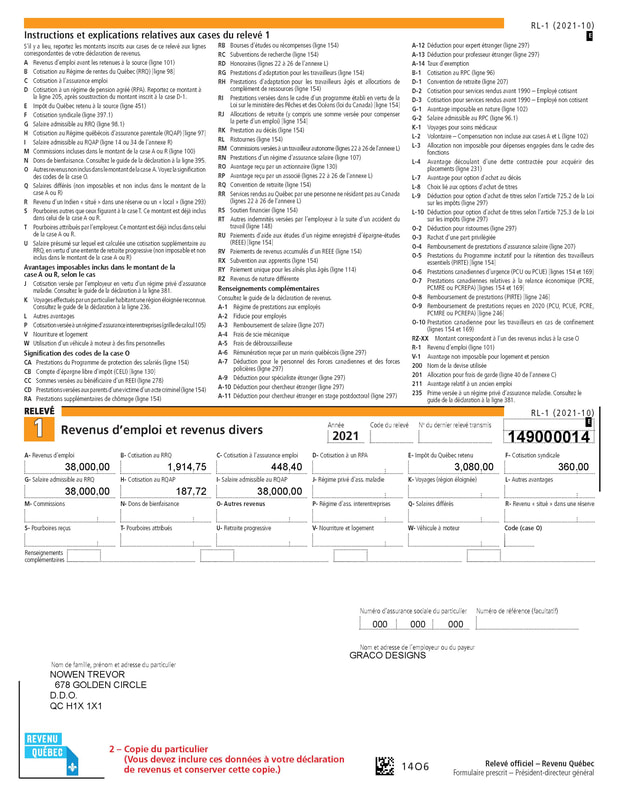

The T-4 and RL-1 Forms

Employers are required to report wages and deductions both to each employee and to the local office of CRA and MRQ. On or before the last day of February, the employer must give each employee a T-4 and RL-1 Summary, a statement that tells the employee:

On or before the last day of February the employer must forward to the district taxation offices copies of the employee's T-4 and RL-1slips, plus a T-4 and RL-1 summaries that summarize the information contained on the employee's T-4 and RL-1 slips. The T-4 and RL-1 slips form are shown HERE

- Total wages for the preceding year.

- Taxable benefits received from the employer.

- Income taxes withheld.

- Deductions for registered pension plan.

- Canada Pension Plan contributions.

- Employment insurance deductions.

On or before the last day of February the employer must forward to the district taxation offices copies of the employee's T-4 and RL-1slips, plus a T-4 and RL-1 summaries that summarize the information contained on the employee's T-4 and RL-1 slips. The T-4 and RL-1 slips form are shown HERE

|

|

Top Payroll Job Opportunities

PAYROLL SPECIALIST

What does a payroll specialist do? A payroll specialist works in a company’s accounting department to manage all aspects of timesheet and payroll processing. The key skills of a payroll specialist are accuracy and timeliness. The role includes:

PAYROLL MANAGER

A payroll manager is a finance and human resources business professional. A payroll position description for payroll manager might include these duties:

PAYROLL CLERK

Payroll Clerk is one of the most common entry level payroll job titles. A Payroll Clerk (sometimes called a payroll assistant) performs a range of supportive duties. Their main focus is on payroll processing and data entry. A payroll clerk:

PAYROLL ADMINISTRATOR

A payroll administrator assists employees who have issues with their pay or need to change their records. A payroll administrator also provides information to employees about salaries and benefits. Other duties include:

PAYROLL PROCESSOR

A payroll processor validates employee work hours and calculates wages. They ensure employees are paid accurately and might also deal with mistakes or complaints by following up with employees. In many organizations, the payroll processor creates and maintains payroll information for all employees.

What does a payroll specialist do? A payroll specialist works in a company’s accounting department to manage all aspects of timesheet and payroll processing. The key skills of a payroll specialist are accuracy and timeliness. The role includes:

- maintaining employee salary databases

- managing company budget and expenses

- coordinating with other departments, managers and employees to improve payroll systems

PAYROLL MANAGER

A payroll manager is a finance and human resources business professional. A payroll position description for payroll manager might include these duties:

- preparing and distributing all aspects of employee payments

- maintaining payroll records and calculating taxes

- balancing payroll accounts

- providing support to a payroll team

- creating payroll procedures and policies

- providing training to their team

PAYROLL CLERK

Payroll Clerk is one of the most common entry level payroll job titles. A Payroll Clerk (sometimes called a payroll assistant) performs a range of supportive duties. Their main focus is on payroll processing and data entry. A payroll clerk:

- pays close attention to details.

- presents a good understanding of math and computer skills.

- distributes paycheques and statements to managers.

- answers questions from employees and vendors

PAYROLL ADMINISTRATOR

A payroll administrator assists employees who have issues with their pay or need to change their records. A payroll administrator also provides information to employees about salaries and benefits. Other duties include:

- issuing payments

- auditing and processing taxes (or other deductions)

- keeping organized data record

PAYROLL PROCESSOR

A payroll processor validates employee work hours and calculates wages. They ensure employees are paid accurately and might also deal with mistakes or complaints by following up with employees. In many organizations, the payroll processor creates and maintains payroll information for all employees.