TIMEKEEPING

Compiling a record of the time worked by each employee is called timekeeping. The method used to compile such a record depends on the nature of the company's business and the number of its employees. In a very small business, timekeeping may consist of no more than notations of each employee's working time made in a memorandum book by the manager or owner.

In many companies, however, time clocks are used to record on clock cards each employee's time of arrival and departure. At the beginning of each payroll period, a clock timecard for each employee is placed in a rack for use by the employee. Upon arriving at work, each employee takes his or her card from the rack and places it in a slot in the time clock. This activates the clock to stamp the date and arrival time on the card. The employee then returns the card to the rack.

Upon leaving the plant, store, or office for lunch or at the end of the day, the procedure is repeated. The employee takes the card from the rack, places it in the clock, and the time of departure is automatically stamped, As a result, at the end of each period, the card shows the hours the employee was at work..

In many companies, however, time clocks are used to record on clock cards each employee's time of arrival and departure. At the beginning of each payroll period, a clock timecard for each employee is placed in a rack for use by the employee. Upon arriving at work, each employee takes his or her card from the rack and places it in a slot in the time clock. This activates the clock to stamp the date and arrival time on the card. The employee then returns the card to the rack.

Upon leaving the plant, store, or office for lunch or at the end of the day, the procedure is repeated. The employee takes the card from the rack, places it in the clock, and the time of departure is automatically stamped, As a result, at the end of each period, the card shows the hours the employee was at work..

TIME CLOCKS & TIMECARDS

TIMECARDS

Calculating your employees’ timecards accurately is crucial to your business. Not only does it ensure you’re paying your employees the right amount, but it also helps management make sure they are not scheduling anyone for too many or too few hours, and it allows them to understand what staffing levels their businesses need to function at their best.

Small business owners may find that calculating timecards manually works well for them initially, especially if they have a small number of hourly employees and few work hours to track. Even more established businesses that are using Excel spreadsheets, timesheet calculators, or other time tracking methods for calculating hours should know how math works. That way, even with a computer, they will be able to spot and correct any inevitable errors.

Some employers – particularly those with large payrolls – use a computerized timekeeping system, which transfers employees’ time worked into a payroll software and eliminates manual calculation.

Otherwise, the payroll clerk manually calculates the timecards before processing the payroll. In the latter case, some general rules apply.

Small business owners may find that calculating timecards manually works well for them initially, especially if they have a small number of hourly employees and few work hours to track. Even more established businesses that are using Excel spreadsheets, timesheet calculators, or other time tracking methods for calculating hours should know how math works. That way, even with a computer, they will be able to spot and correct any inevitable errors.

Some employers – particularly those with large payrolls – use a computerized timekeeping system, which transfers employees’ time worked into a payroll software and eliminates manual calculation.

Otherwise, the payroll clerk manually calculates the timecards before processing the payroll. In the latter case, some general rules apply.

SAMPLE TIMECARDS

|

|

|

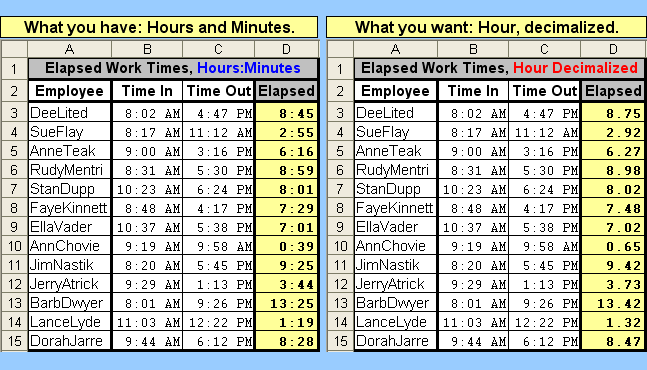

Converting Minutes to Decimals Hours

Decimal Clock

|

Conversion from Minutes to Decimal Hours

Example: How to Calculate Hours Worked

|

HOW TO DO THE MATH FOR TIMECARDS

- Manually tracking employee hours by hand is an old method, but it works. Here’s how to do it.

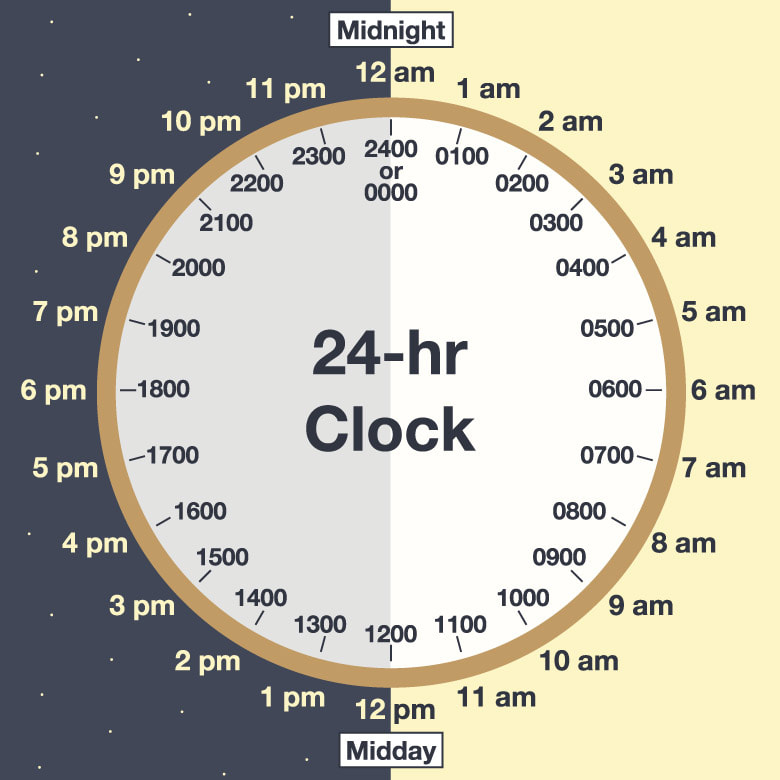

- Convert an employee’s start and end hours for the day, as well as any unpaid break time, to 24-hour time, also known as military time.

- For example, two employees began working at 9:22 a.m., took a lunch break from 12:30-1:15 p.m., and ended their day at 5:08 p.m. In a 24-hour time span, the hours past 12 p.m. must be converted, so 1:15 p.m. would 13:15 p.m.

- Convert the minutes into decimal format—instead of minutes out of 60, make them percentages of 100. To do this, you can either use a chart or simply divide the minutes by 60.

- In this example, this means your employee’s clock-IN and clock-OUT times become 09.37 and 12.50 for the first half of their shift and 13.25 and 17.13 for the second half of their shift.

- Subtract the employee’s shift start times from the end times.

- 12.50 – 09.37 = 03.13 and 17.13 – 13.25 = 03.88

- Add the working hours from step three together to get the total for the day.

- 03.13 + 03.88 = 07.01

24-Hour Clock

MANUALLY CALCULATING TIMECARDS

Step 1

Rounding Time Up and Down

Round employees’ time up and down to the nearest quarter-hour. Specifically, round minutes from one to seven down, and minutes from eight to 14 up, to the closest quarter hour. For example, round 8:24 up to 8:30 a.m. and 16:02 p.m. down to 16.00 p.m.

Step 2

Conversion of Time to Decimals

Convert employees’ time to decimals as follows: 1/4 of an hour equals 0.25, 1/2 of an hour equals 0.50, and 3/4 of an hour equals 0.75. For example, say the timecard shows seven hours and 30 minutes worked on Monday and eight hours and 45 minutes worked on Tuesday. Convert the former to 7.50 hours and the latter to 8.75 hours.

Step 3

Meal/Break Periods

Count short breaks – generally lasting five to 15 minutes – as paid time, and lunch breaks – typically lasting at least 30 minutes – as unpaid time. In many cases, if the province requires an employer give paid breaks or if the employer provides it by policy, the employer might not require employees to clock in and out for breaks, only for lunch. In this case, subtract only the employee’s meal period from the employees' timecard and pay them for the remaining hours.

Step 4

Calculating Hours Worked

Timecards are weekly; therefore, whether an employee is paid on a weekly, biweekly or semimonthly basis, when calculating overtime, consider the employees' hours worked for the day or week rather than their payroll frequency.

Step 5

Consideration of Overtime Rules and Date of Payment

Apply the labor standards overtime rules, such as overtime pay for work hours that exceed a 40 hours per week.

Repeat steps 1 to 5 to calculate the timecards for the remaining employees.

Rounding Time Up and Down

Round employees’ time up and down to the nearest quarter-hour. Specifically, round minutes from one to seven down, and minutes from eight to 14 up, to the closest quarter hour. For example, round 8:24 up to 8:30 a.m. and 16:02 p.m. down to 16.00 p.m.

Step 2

Conversion of Time to Decimals

Convert employees’ time to decimals as follows: 1/4 of an hour equals 0.25, 1/2 of an hour equals 0.50, and 3/4 of an hour equals 0.75. For example, say the timecard shows seven hours and 30 minutes worked on Monday and eight hours and 45 minutes worked on Tuesday. Convert the former to 7.50 hours and the latter to 8.75 hours.

Step 3

Meal/Break Periods

Count short breaks – generally lasting five to 15 minutes – as paid time, and lunch breaks – typically lasting at least 30 minutes – as unpaid time. In many cases, if the province requires an employer give paid breaks or if the employer provides it by policy, the employer might not require employees to clock in and out for breaks, only for lunch. In this case, subtract only the employee’s meal period from the employees' timecard and pay them for the remaining hours.

Step 4

Calculating Hours Worked

Timecards are weekly; therefore, whether an employee is paid on a weekly, biweekly or semimonthly basis, when calculating overtime, consider the employees' hours worked for the day or week rather than their payroll frequency.

Step 5

Consideration of Overtime Rules and Date of Payment

Apply the labor standards overtime rules, such as overtime pay for work hours that exceed a 40 hours per week.

Repeat steps 1 to 5 to calculate the timecards for the remaining employees.

Marcof’s Furniture Company

Completing Marcof’s Furniture Payroll

Now we are ready to see how a business computes and records the earnings of its employees and the related taxes to be deducted in computing the employees' net pay. Marcof’s Furniture Company is used to illustrate typical payroll procedures and records. This is a wholesale furniture company that purchases furniture and appliances from manufacturers and other wholesalers, and in turn sells to several retailers.

The company also employs four employees who work in the office and three who work in the warehouse. Because of the size of the company, the owner believes it more beneficial to pay all employees on a weekly basis. All office staff and warehouse workers are hourly-paid and therefore receive their wages weekly. All employees are paid each Monday for wages and salaries earned during the week that ended on the preceding Saturday.

The employees are subject to the QPP, QPIP, employment insurance premiums, federal and provincial income taxes The owner, Elizabeth Marcof oversees the day-to-day operations of the company, as well as handles advertising, promotion, and the purchasing of all inventory items. She withdraws a portion of the profits from time to time to take care of her living expenses. Because she is the owner of a sole proprietorship, her drawings are not treated as salaries or wages. The firm itself is subject to QPP, QPIP and employment insurance taxes. In addition, the business is required to carry workers' compensation insurance and contribute to the Quebec health service fund.

The company also employs four employees who work in the office and three who work in the warehouse. Because of the size of the company, the owner believes it more beneficial to pay all employees on a weekly basis. All office staff and warehouse workers are hourly-paid and therefore receive their wages weekly. All employees are paid each Monday for wages and salaries earned during the week that ended on the preceding Saturday.

The employees are subject to the QPP, QPIP, employment insurance premiums, federal and provincial income taxes The owner, Elizabeth Marcof oversees the day-to-day operations of the company, as well as handles advertising, promotion, and the purchasing of all inventory items. She withdraws a portion of the profits from time to time to take care of her living expenses. Because she is the owner of a sole proprietorship, her drawings are not treated as salaries or wages. The firm itself is subject to QPP, QPIP and employment insurance taxes. In addition, the business is required to carry workers' compensation insurance and contribute to the Quebec health service fund.