|

EMPLOYEES' PAYROLL RECORDS |

Overview

Payroll Records constitute anything and everything related to the information about the company’s employees. It depicts the amount for which the employees are paid during each period. Naturally, the period differs from company to company. It can be daily, weekly, bi-weekly, semi-monthly, monthly, or any period which suits the company’s pay period.

Sample Employees' Earning Records

|

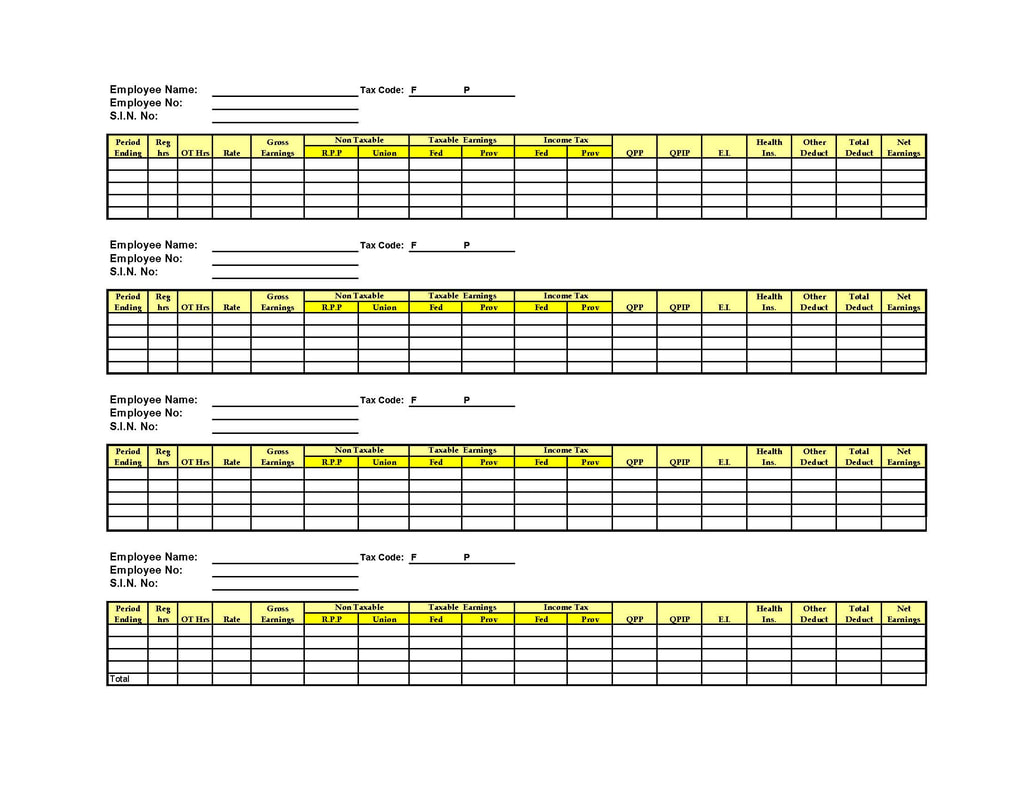

Blank Employees Earnings Records

|

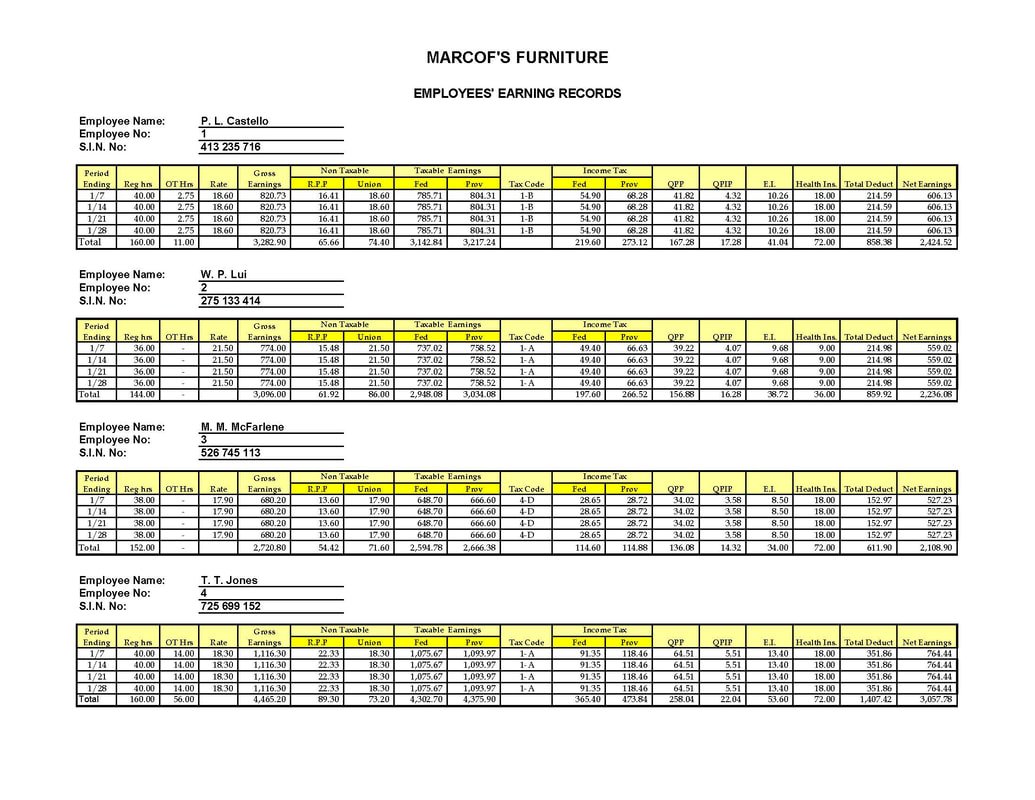

Completed Employees' Earnings Records

|

What are Payroll Records?

A payroll record can be defined as a list of all the employees of that company in which every information related to the payments made to the employees which they are entitled to receive, such as salaries, wages, bonuses, taxes, etc. are recorded so that at every interval there can be a proper track of each payment which are paid to those employees from the employer’s point of view. If a discrepancy occurs, then the same could be pointed out easily from the records.

What Is Included In Payroll Record?

- The foremost information is gross pay, which is the main in-hand amount shown first before making any deduction from it. Gross pay is calculated by multiplying the hourly pay rate by the number of days worked.

- The next information would be deductions, which are of two types: mandatory deductions and voluntary deductions. Several taxes include professional tax, provident fund contribution from the employee’s portion, etc.

- The last is the net pay, the final amount after making all the deductions credited to the employee’s account.

Employee's Individual Earnings Record

An Employee's Individual Earnings Record, as shown below, provides for each employee, in one record, a full year's summary of the employee's working time, gross earnings, deductions, and net pay. In addition, it accumulates information that:

The payroll information on an Employee's Individual Earnings Record is taken from the Payroll Register. The information as to earnings, deductions, and net pay is first recorded on a single line in the Payroll Register. Then, each pay period the information is posted from the Payroll Register to the earnings record.

Note the last column of the record. It shows an employee's cumulative earnings and is used to determine when the earnings reach the maximum amounts taxed and are no longer subject to the various payroll taxes.

- Serves as a basis for the employer's payroll tax returns.

- Indicates when an employee's earnings have reached the maximum amounts for QPP and EI deductions.

- Supplies data for the T4 and RL-1 slips, which must be given to the employee at the end of the year.

The payroll information on an Employee's Individual Earnings Record is taken from the Payroll Register. The information as to earnings, deductions, and net pay is first recorded on a single line in the Payroll Register. Then, each pay period the information is posted from the Payroll Register to the earnings record.

Note the last column of the record. It shows an employee's cumulative earnings and is used to determine when the earnings reach the maximum amounts taxed and are no longer subject to the various payroll taxes.

Managing an Employee's Payroll Record

At the beginning of each year, or when a new employee is hired during the year, an individual earnings record is set up for each worker. This record contains the employee's name, address, social insurance number, date of birth, tax claim code, rate of pay, and any other information that may be needed in computing earnings and filing necessary tax reports. The details for each pay period are posted to the employee's individual earnings record from the payroll register.

Note that the details shown in this record include the payroll date (entered in the Week Ended column), the date paid, the regular and overtime hours worked, the earnings (broken down into regular earnings and overtime premium, as indicated in the payroll register), each deduction, and the net pay. The cumulative total earnings after each payroll agrees with the balance shown for each employee in column I of the payroll register. It is recomputed each time a payroll entry is made in an earnings record.

Note that the details shown in this record include the payroll date (entered in the Week Ended column), the date paid, the regular and overtime hours worked, the earnings (broken down into regular earnings and overtime premium, as indicated in the payroll register), each deduction, and the net pay. The cumulative total earnings after each payroll agrees with the balance shown for each employee in column I of the payroll register. It is recomputed each time a payroll entry is made in an earnings record.

Where To Keep Payroll Records

Companies must keep records at their place of business or their residence in Canada, unless the Canada Revenue Agency (CRA) gives them written permission to keep them elsewhere.

Note

Records kept outside of Canada and accessed electronically from Canada are not considered to be records kept in Canada.

The CRA will not give permission to keep records outside of Canada to:

For permission to keep records elsewhere, a company must write to its tax services office. After reviewing its situation, the CRA will provide its written permission. The CRA's written permission will specify any terms and conditions.

If the CRA gives a company permission to keep your records outside of Canada, it must make them available upon request in Canada for review by the CRA.

The CRA may give permission for a company to keep its electronic records outside of Canada. If so, the CRA may accept copies if:

If you keep your records on servers located outside Canada, you must access the servers or arrange for your staff to access the servers and provide the electronic system records required by CRA officials.

Note

Records kept outside of Canada and accessed electronically from Canada are not considered to be records kept in Canada.

The CRA will not give permission to keep records outside of Canada to:

- registered charities

- registered Canadian amateur athletic associations.

- Canadian municipalities

- public bodies performing a function of government.

- housing corporations resident of Canada and exempt from tax under the Income Tax Act

For permission to keep records elsewhere, a company must write to its tax services office. After reviewing its situation, the CRA will provide its written permission. The CRA's written permission will specify any terms and conditions.

If the CRA gives a company permission to keep your records outside of Canada, it must make them available upon request in Canada for review by the CRA.

The CRA may give permission for a company to keep its electronic records outside of Canada. If so, the CRA may accept copies if:

- the CRA is satisfied that the copies of the records are true copies.

- they are made available to CRA officials in Canada in an electronic format readable by CRA software.

- they show enough details to support the returns filed with the CRA.

If you keep your records on servers located outside Canada, you must access the servers or arrange for your staff to access the servers and provide the electronic system records required by CRA officials.

How Long to Keep Payroll Records?

The employer should preserve the certified payroll record for six years according to the Income Tax Act with other documentation like sales and purchase records, etc. In addition, the records on which the wage computation is recorded should be retained for two years, i.e., timecards, tables of wage rate, work, time schedules, and other records of addition and subtraction from the wages and salaries.

These records should be open for inspection by the division’s in-charge, who may ask the employer to make necessary changes. These records should be kept in the Central Record Office/at employment.

These records should be open for inspection by the division’s in-charge, who may ask the employer to make necessary changes. These records should be kept in the Central Record Office/at employment.

Advantages & Disadvantages of Payroll Recordkeeping

Advantages

Disadvantages

- The system provides us with easy calculations, making the entire pay mechanism very lucid.

- This facilitates accuracy so that the correct amount can be paid out, and it won’t cause any further discrepancies.

- The computerized payroll system reduces the chances of errors and makes an easy flow of data and information that can be trusted and re-used.

- This system has an appropriate structure for deductions and payments that are automatically set in the record to be used to calculate salaries/wages.

- This can be treated as a safe backup option, and any information demanded retrospectively; the records can be useful then.

- The record-keeping of the payroll system reinstates the faith in the employees that a properly organized and documented form is maintained for their earnings. Whatever deduction is made, proper proof will be shown. In the future, if an employee demands a payroll record, the company would be in a position to present them with proper backup available to them.

- This system is a cost-effective mechanism through which every penny paid/deducted to the employee can be tracked. The system gives back to the organization to maintain the data correctly and prevent the organization from any future hassles.

- As the system is very cost-effective from the previous point, it saves time greatly because it does not allow any discrepancies and prevents any duplicity of work. For every fixed period of the interval, the correct data allows the organization for an error-free future of work.

- In case of any inspection/audit/background check, if any authority demands any personnel records, this can be proof of evidence. It will not only be a savior for a well-maintained system but also will make a difference in the goodwill of the company.

- This can be a major tool for forecasting the company. A company’s major part of profits pays salaries and wages to its employees. If an estimated budget can be predicted for a future period, it can be a great tool for forecasting future costs and budgets for the company.

- The organization can well plan its costs and then make out the reserves/investments accordingly.

Disadvantages

- A payroll record holds data, and information can be at risk for data security, theft, or data leak. The sensitive information can be made open if it is not well protected.

- The second disadvantage can be cyber fraud, which is almost very common. The rivalry amongst companies can be a root source of this problem.

- Information access/control cannot be given to all. Only the person in charge of the payroll record should be familiar with the information. The person should be trustworthy enough not to leak out the company’s sensitive data.

- The last but not the least disadvantage can be the cost involved. The software, skilled operators, and the infrastructure required to set up the payroll record system are huge, which can be a barrier for a few organizations to meet up.