|

THE PAYROLL REGISTER |

What is the Payroll Register?

Payroll has a lot of moving parts to keep track of employee hours, gross pay, net pay, payroll taxes, employee deductions, employer contributions, and the list goes on. Seeing all that information in one place would be a dream come true, right?

Juggling all the aspects of the payroll process can be one of the most overwhelming aspects of running a small business. Manually balancing and aggregating the employees’ wages and personal information can be a time-consuming task that detracts from time and energy spent elsewhere. In addition to keeping track of hours worked, management also needs to keep meticulous records for taxes, compliance with provincial and federal laws. That’s where the payroll register comes in. So, what is a payroll register, and what exactly does it do?

A payroll register is a valuable tool that records employee wage information for each pay period and pay date. It’s useful for record-keeping in a business and has legal implications if not kept correctly. A summary of all payroll activity is an excellent way to look at the payroll register report. It differs from other reports, such as a paycheque history report or a payroll details report.

Generally, a payroll register lists the following information about each employee:

Juggling all the aspects of the payroll process can be one of the most overwhelming aspects of running a small business. Manually balancing and aggregating the employees’ wages and personal information can be a time-consuming task that detracts from time and energy spent elsewhere. In addition to keeping track of hours worked, management also needs to keep meticulous records for taxes, compliance with provincial and federal laws. That’s where the payroll register comes in. So, what is a payroll register, and what exactly does it do?

A payroll register is a valuable tool that records employee wage information for each pay period and pay date. It’s useful for record-keeping in a business and has legal implications if not kept correctly. A summary of all payroll activity is an excellent way to look at the payroll register report. It differs from other reports, such as a paycheque history report or a payroll details report.

Generally, a payroll register lists the following information about each employee:

- Gross pay

- Net pay

- Payroll taxes

- Employee deductions (e.g., health insurance)

Blank Payroll Register

Steps to Complete Payroll Register

The steps in completing the payroll register are summarized below. Refer to the columns in the payroll register you read the descriptions given below for each column of the register.

The column totals from the payroll register supply all the necessary figures to prepare the journal entries to record the payroll. This will be discussed later.

- Columns A, B, C, D and F. The employees’ number column (A), social insurance number in column (B) and their name in (C), followed by total regular hours worked for the period in Column (D), and pay rate column (F) can be entered in the register in advance to save time in the payroll preparation. In a computerized payroll system, this information would be stored in the computer and automatically retrieved when the payroll is entered.

- Column D. From the completed time records, the total hours worked in the current period are entered in column D.

- Columns D, E, F, and G. Gross earnings computations are entered in the Gross Earnings section. These amounts are classified according to regular earnings column (D) and overtime hours column (E) multiplied by the pay rate in column (F). The total of which is entered in the payroll register--the sum of these earnings is entered in column (G), Gross Earnings.

- Columns H, and I. The non-taxable amounts are entered in these columns. In column (H) RPP and Union in column (I). These amounts will reduce the employees’ tax liability.

- Columns J and K. In these columns the federal and provincial income taxes payable are calculated. In column J the federal income tax payable is determined by subtracting RPP and Union from the gross earnings. While the provincial income tax payable is calculated by subtracting only the union from the gross earnings.

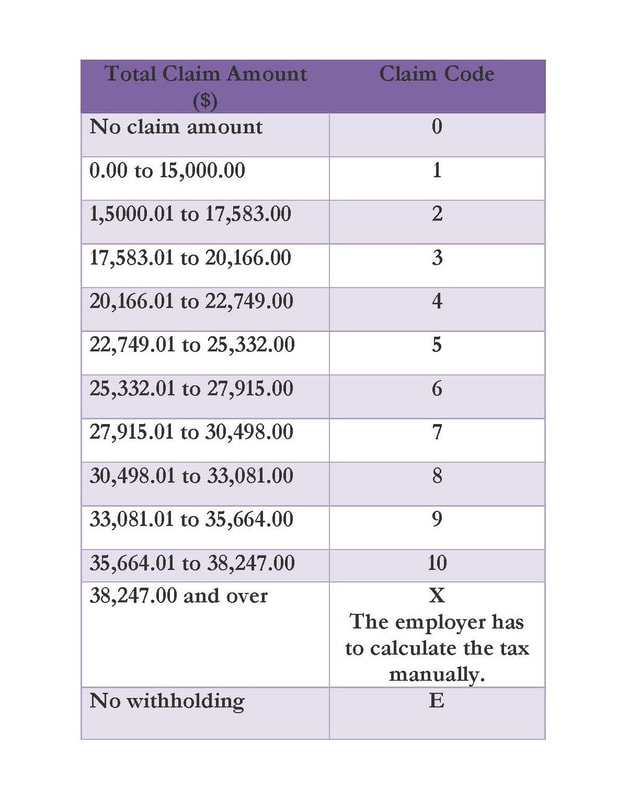

- Column L. This column displays the employees’ federal and provincial claim code. To determine the tax credits, employees must complete the TD1 and TP-1 to determine their tax codes. These codes are used to determine their tax liability.

- Columns M, N, 0, P, Q, and R. The withholding amounts are entered in the payroll register. The federal income tax in column (M), provincial in column (N), QPP column (O), QPIP column (P), EI column(Q), other deductions--health insurance, etc.--columns (R). Most payroll registers also contain an additional column entitled "Other" in which non-recurring withholdings may be recorded.

- Columns S, T and U. Next the total deductions—column (S)--for each employee is subtracted from the gross earnings to determine the employees’ net earnings. This figure is recorded in the Net Earnings column (T). Column (U) the cheque number used to pay the net amount due to each employee is recorded.

- When the payroll information for all employees has been entered in the payroll register, the columns are totalled as shown in the completed payroll register in the next section.

- Rows G12:N18. In this area the employer’s costs are calculated EI, QPP, QPIP, QHSF. In addition, the total amount of federal and provincial remittances is calculated and remitted to the respective governments by the 15th of the month following. These remittances include both the employees’ deductions at source (DAS) and the employers’ costs. Furthermore, the employers would also remit amounts to the other agencies for RPP, Health Insurance, Union etc. (These deductions are optional and may not be necessary for all companies).

The column totals from the payroll register supply all the necessary figures to prepare the journal entries to record the payroll. This will be discussed later.

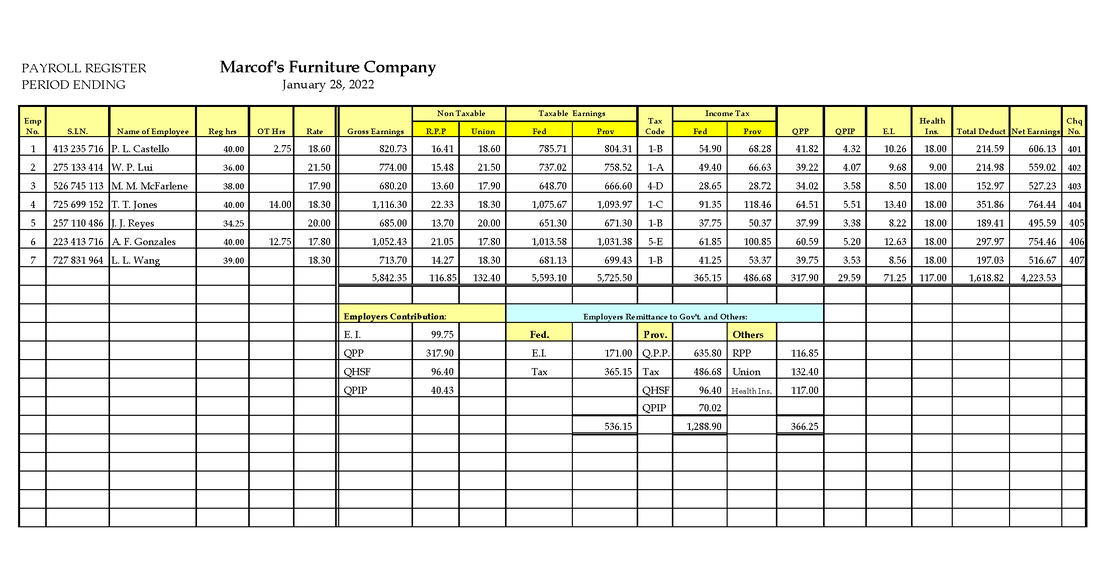

Completed Payroll Register

Entering Pay in The Payroll Register

Each pay period the total hours worked as compiled on timecards or by other means are summarized in a Payroll Register, an example of which is shown below. The illustrated register is for a weekly period and shows the payroll date. For each employee on a separate line.

In above example the column under the heading Reg. Hrs. shows the hours worked for each employee. The total of each employee’s hours is entered in the column Total Hours. If hours include overtime these are entered in a column headed OT Hrs.

The Regular Pay Rate shows the hourly rate for each employee. Total hours worked by each employee multiplied by the regular pay rate equal regular pay. Overtime hours multiplied by overtime premium rate (50% in this case) equals overtime premium pay. And regular pay plus overtime premium pay is the employee's gross pay.

In the Non taxable column are the allowable amounts the individual can use to reduce their tax liability. These amounts will be discussed later on the website under the headings Federal/Provincial -reducing remuneration subject to income tax. The amounts withheld from each employee's gross pay are recorded under the respective columns the of the payroll register. For example, you determine the income tax deductions by matching the gross pay of each employee to the tax deduction tables and then enter the results in the tax deduction column. Income tax deductions are based on the gross pay less the amounts deducted from RPP and Union for federal government, and only Union for the provincial government. The tax tables allow for these adjustments and separate books are available for each province. The income tax deductions are based on the employees being resident in Quebec.

In above example the column under the heading Reg. Hrs. shows the hours worked for each employee. The total of each employee’s hours is entered in the column Total Hours. If hours include overtime these are entered in a column headed OT Hrs.

The Regular Pay Rate shows the hourly rate for each employee. Total hours worked by each employee multiplied by the regular pay rate equal regular pay. Overtime hours multiplied by overtime premium rate (50% in this case) equals overtime premium pay. And regular pay plus overtime premium pay is the employee's gross pay.

In the Non taxable column are the allowable amounts the individual can use to reduce their tax liability. These amounts will be discussed later on the website under the headings Federal/Provincial -reducing remuneration subject to income tax. The amounts withheld from each employee's gross pay are recorded under the respective columns the of the payroll register. For example, you determine the income tax deductions by matching the gross pay of each employee to the tax deduction tables and then enter the results in the tax deduction column. Income tax deductions are based on the gross pay less the amounts deducted from RPP and Union for federal government, and only Union for the provincial government. The tax tables allow for these adjustments and separate books are available for each province. The income tax deductions are based on the employees being resident in Quebec.

Mandatory Employees' Withholdings

Employees' Income Tax Deductions

With a few exceptions, employers are required to calculate, collect, and remit to the federal and provincial governments the income taxes of their employees. Historically, when the first federal income tax law became effective in 1917, it applied to only a few individuals having high earnings. It was not until World War II that income taxes were levied on substantially all wage earners. At that time Parliament recognized that many individual wage earners could not be expected to save sufficient money with which to pay their income taxes once each year.

Consequently, Parliament instituted a system of pay-as-you-go withholding of taxes at their source each payday. This pay-as-you-go withholding of employee income taxes requires an employer to act as a tax collecting agent of the federal government. Failure to cooperate results in severe consequences, as illustrated before on this website.

The amount of income taxes to be withheld from an employee's wages is determined by his or her wages and the amount of personal tax credits. Each individual is entitled, in 2023, to some or all of the following annual amounts that are subject to tax credits (as applicable):

Consequently, Parliament instituted a system of pay-as-you-go withholding of taxes at their source each payday. This pay-as-you-go withholding of employee income taxes requires an employer to act as a tax collecting agent of the federal government. Failure to cooperate results in severe consequences, as illustrated before on this website.

The amount of income taxes to be withheld from an employee's wages is determined by his or her wages and the amount of personal tax credits. Each individual is entitled, in 2023, to some or all of the following annual amounts that are subject to tax credits (as applicable):

Claiming Personal Tax Credits

The amount of income tax to be withheld from an employee's earnings generally depends on the amount of income during the pay period, the length of the pay period, the number of allowable tax-deductible credits, and marital status, In brief, a person is ordinarily entitled to a basic personal tax credit for himself or herself, one for a spouse.

If the employee desires, he or she may instruct the employer to withhold in each payroll period a specified amount of income tax above the amount required by law. This practice reduces the possibility that a balance may be due when the individual files his or her yearly income tax return.

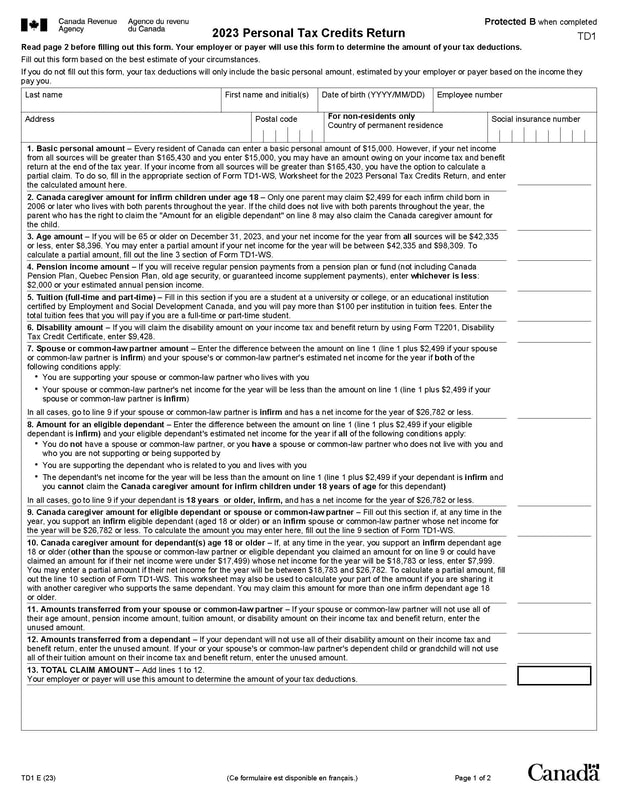

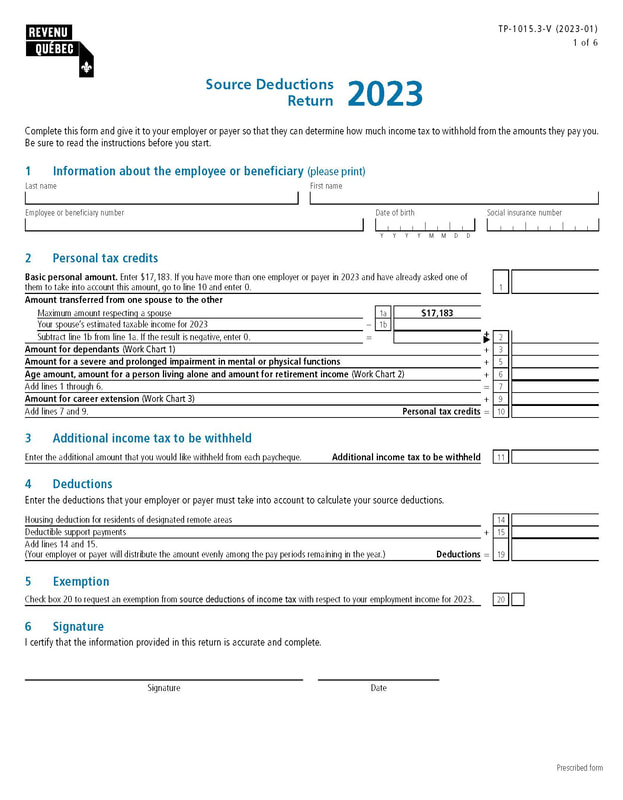

Employees claim the number of personal tax credits to which they are entitled by completing two Personal Tax Credits Return TD1 forms-one federal and the other provincial-TPI (These forms are filed with the employer.

If an employee fails to file a Form TD1 or TP-1 at both the federal level and the provincial level, the employer must withhold income tax from the employee's wages as though there were no exemption allowances. If the number of exemptions decreases, the employee must file new federal and provincial TD1 and TP-1 forms within 10 days, If the number of exemption allowances increases, the employee may file an amended certificate but is not required to do so.

The total of each taxpayer's personal tax credits is deducted from income to determine the level of income tax deductions from the individual's gross pay. For example, based on rates effective January 1, 2023, a Quebec resident with a gross weekly salary of $1,200 and personal tax credits of $15,000 (2023 net claim Code 1 on the TDI form) would have $106.15 of income taxes withheld. Another individual with the same gross salary but with personal tax credits of $23,371 (claim code 5) would have $84.40 withheld. Employers withhold income tax owed by each employee every payday based on an employee's completed Personal Tax Credit Return, Form TD1. The taxpayer must file a revised Form TDI each time the exemptions change during a year. The electronic TD 1 and TP1 forms are shown below.

If the employee desires, he or she may instruct the employer to withhold in each payroll period a specified amount of income tax above the amount required by law. This practice reduces the possibility that a balance may be due when the individual files his or her yearly income tax return.

Employees claim the number of personal tax credits to which they are entitled by completing two Personal Tax Credits Return TD1 forms-one federal and the other provincial-TPI (These forms are filed with the employer.

If an employee fails to file a Form TD1 or TP-1 at both the federal level and the provincial level, the employer must withhold income tax from the employee's wages as though there were no exemption allowances. If the number of exemptions decreases, the employee must file new federal and provincial TD1 and TP-1 forms within 10 days, If the number of exemption allowances increases, the employee may file an amended certificate but is not required to do so.

The total of each taxpayer's personal tax credits is deducted from income to determine the level of income tax deductions from the individual's gross pay. For example, based on rates effective January 1, 2023, a Quebec resident with a gross weekly salary of $1,200 and personal tax credits of $15,000 (2023 net claim Code 1 on the TDI form) would have $106.15 of income taxes withheld. Another individual with the same gross salary but with personal tax credits of $23,371 (claim code 5) would have $84.40 withheld. Employers withhold income tax owed by each employee every payday based on an employee's completed Personal Tax Credit Return, Form TD1. The taxpayer must file a revised Form TDI each time the exemptions change during a year. The electronic TD 1 and TP1 forms are shown below.

Federal Government TD1 - Page 1

|

Quebec Government TP-1 - Page #1

|

In determining the amounts of income taxes to be withheld from the wages of employees, employers normally use payroll deductions tables provided by Canadian Revenue Agency (CRA). The to-be-withheld amount for federal provincial income taxes except for the province of Quebec, which levies and collects its own income tax and its own pension plan contributions. Provincial income tax rates vary from province to province.

Therefore, for consistency, some examples on the website will be illustrated by using the tax tables based on Federal income taxes to be withheld for Quebec's residents. However, with the final payroll illustration I will be using both federal and provincial tables to prepare the payroll for a Quebec company. In addition to determining and withholding income taxes from each employee's wages every payday, employers are required to remit the withheld taxes to the Receiver General for Canada each month.

Therefore, for consistency, some examples on the website will be illustrated by using the tax tables based on Federal income taxes to be withheld for Quebec's residents. However, with the final payroll illustration I will be using both federal and provincial tables to prepare the payroll for a Quebec company. In addition to determining and withholding income taxes from each employee's wages every payday, employers are required to remit the withheld taxes to the Receiver General for Canada each month.

|

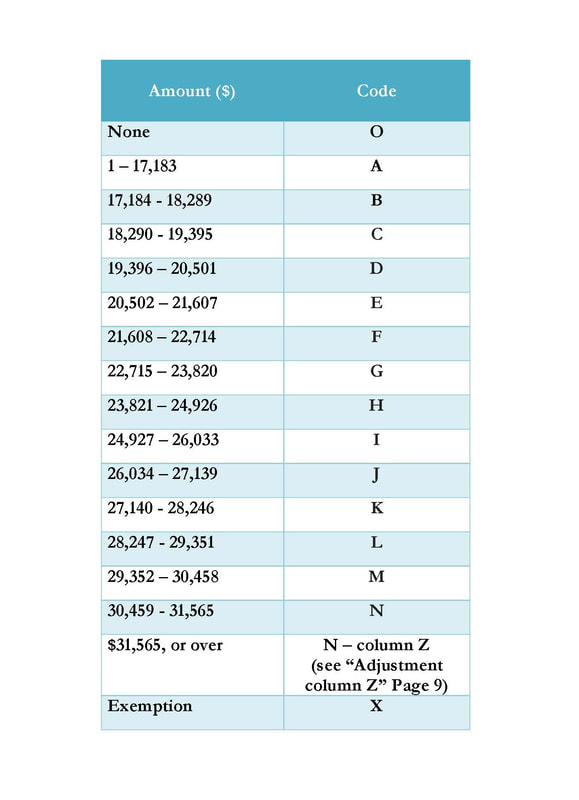

Federal Claim Codes

|

Provincial Claim Codes

|

Different Status - Different Tax Code

|

Single

|

Single Parent

|

Couple

|

Caregiver

|

Family

|

Senior Citizen

|

DETERMINING TAXABLE INCOME

Federal Government

Reducing Remuneration Subject to Income Tax

Certain amounts that employers can deduct from the remuneration from their employees’ pay employee, as well as other authorized or claimed amounts, can reduce the amount of remuneration from which they deduct tax for the pay period.

Employers would reduce the employees’ remuneration by the following amounts before calculating their tax:

Employers would reduce the employees’ remuneration by the following amounts before calculating their tax:

- A deduction for living in a prescribed zone.

- An amount that a tax services office has authorized (see Letter of authority).

- An employee has to send Form T1213, Request to Reduce Tax Deductions at Source to CRA to receive a letter of authority or a written request to the appropriate Taxpayer Services Regional Correspondence Centre. The employee should include documents that support their position why less tax should be deducted at source.

Employee's contributions to a registered pension plan (RPP). For details on how to determine the exact amount of these contributions, go to Contributions to a registered pension plan (RPP). - Union dues.

- Employee's contributions to a retirement compensation arrangement (RCA) or certain pension plans. For more information on determining whether an employee can deduct contributions to an RCA.

- Employee's and employer's contributions to a registered retirement savings plan (RRSP) provided you have reasonable grounds to believe the employee can deduct the contribution for the year. For more information, go to RRSP contributions you withhold from remuneration.

- Employee's contributions to a pooled registered pension plan (PRPP), or a similar provincial pension plan, as long as the plan is registered with the Minister of National Revenue, and you have reasonable grounds to believe the employee can deduct the contributions for the year. For more information, go to The Pooled Registered Pension Plan (PRPP).

Provincial Government

Reducing Remuneration Subject to Income Tax

In some cases, employers must subtract certain contributions and deductions from the remuneration subject to source deductions of income tax. For each pay period, reduce an employee's gross remuneration by subtracting:

- registered pension plan (RPP) contributions.

- contributions to a registered retirement savings plan (RRSP), a voluntary retirement savings plan (VRSP) or a pooled registered pension plan (PRPP) that you withhold and remit directly to the plan administrator.

- contributions to a retirement compensation arrangement that you withhold and pay to the retirement compensation arrangement.

- the deduction for the purchase of shares in a labour-sponsored fund;

- the Cooperative Investment Plan (CIP) deduction.

- the travel deduction for residents of designated remote areas

- Employees could claim the deduction for residents of designated remote areas if they lived in a designated remote area (a Northern zone or an intermediate zone) for a period of at least six consecutive months that started or ended in taxation year. The amount they can claim includes the housing deduction and the travel deduction

USING THE DEDUCTION TABLES

Federal Tax Deduction Tables: There are five steps to locating the correct deduction in the federal tax tables. See the illustration below

Provincial Tax Deduction Tables: There are five steps to locating the correct deduction in the provincial tax tables. See the illustration below:

Quebec Employment Insurance Deduction Tables: There are three steps to locating the correct deduction in the Quebec Employment Insurance deduction tables. See the illustration below:

Quebec Employment Insurance Deduction Tables: There are three steps to locating the correct deduction in the Quebec Employment Insurance deduction tables. See the illustration below:

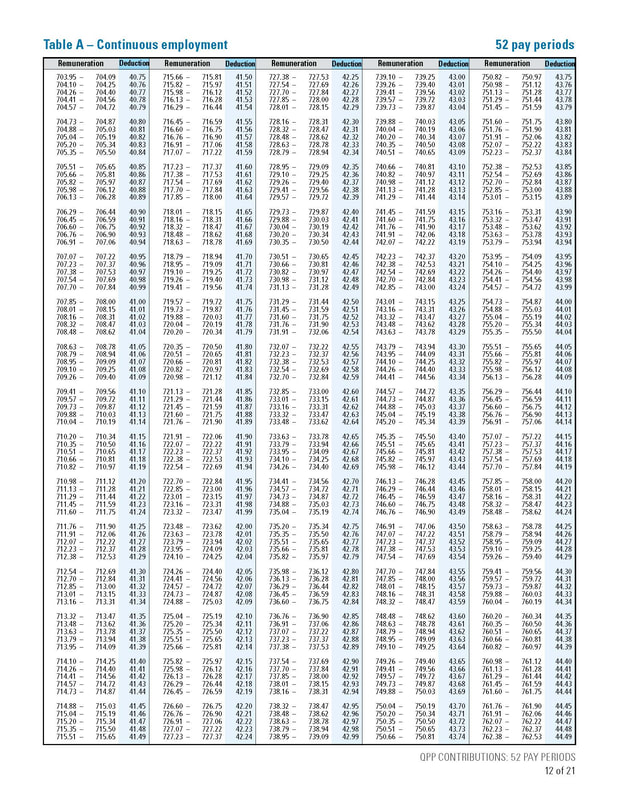

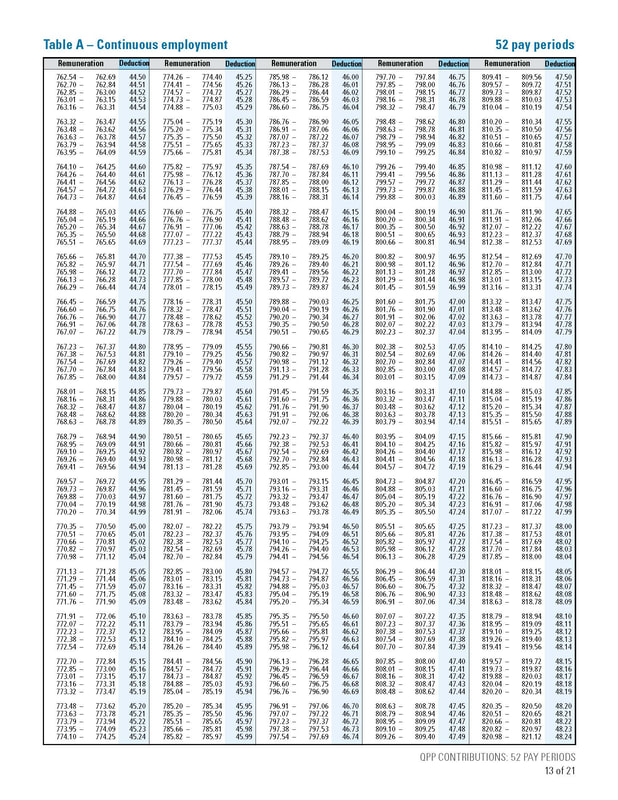

QPP Contribution Deduction Tables: There are four steps to locating the correct deduction in the QPP Contribution Deduction Tables. See the illustration below:

QPIP Contribution Deduction Tables: There are three steps to locating the correct deduction in the QPIP Contribution Deduction Tables. See the illustration below:

These steps will be further demonstrated in class.

Provincial Tax Deduction Tables: There are five steps to locating the correct deduction in the provincial tax tables. See the illustration below:

Quebec Employment Insurance Deduction Tables: There are three steps to locating the correct deduction in the Quebec Employment Insurance deduction tables. See the illustration below:

Quebec Employment Insurance Deduction Tables: There are three steps to locating the correct deduction in the Quebec Employment Insurance deduction tables. See the illustration below:

QPP Contribution Deduction Tables: There are four steps to locating the correct deduction in the QPP Contribution Deduction Tables. See the illustration below:

QPIP Contribution Deduction Tables: There are three steps to locating the correct deduction in the QPIP Contribution Deduction Tables. See the illustration below:

These steps will be further demonstrated in class.

Steps to Follow When Using Deduction Tables

COMPUTING INCOME TAX DEDUCTIONS

How to determine an employee's income tax deduction

A substantial portion of the government's revenue comes from the income tax on individuals. Many rules and regulations are used in determining the amount of income tax that each person must pay. Also keep in mind that rates, rules, and regulations change often; 2023 rates used on this website are for illustrative purposes only. In actual practice, a current edition of the Canada Revenue Agency Payroll Deductions Table would be consulted for up-to-date rates and other information.

Most taxpayers are on a pay-as-you-go basis. This means that an estimate of the income tax due from a person earning a salary or wages must be withheld by the employer and paid to the government periodically-generally while QPP and EI premiums are paid. At the end of each year, the employee files an income tax return. If the amount withheld does not cover the amount of income tax due, the employee pays the balance, if too much has been withheld, the employee will receive a refund.

Several methods can be used to compute the amount of income tax to be withheld from an employee's earnings. However, all except one method requires cumbersome computations. The exception is the wage-bracket table method, which involves the use of tables to determine the amount of tax.

The simplicity of this method explains why it is used almost universally. Payroll Deductions Tables contain withholding tables for weekly, biweekly, semi-monthly, and monthly deductions. Sections of the tables for persons paid weekly are illustrated in Below The steps in determining the amount to be withheld are:

The amount of federal and provincial income taxes to be withheld from the wages of each hourly employee of Marcof’s Furniture is determined in a similar manner from the sections of the weekly wage-bracket withholding tables shown here.

Most taxpayers are on a pay-as-you-go basis. This means that an estimate of the income tax due from a person earning a salary or wages must be withheld by the employer and paid to the government periodically-generally while QPP and EI premiums are paid. At the end of each year, the employee files an income tax return. If the amount withheld does not cover the amount of income tax due, the employee pays the balance, if too much has been withheld, the employee will receive a refund.

Several methods can be used to compute the amount of income tax to be withheld from an employee's earnings. However, all except one method requires cumbersome computations. The exception is the wage-bracket table method, which involves the use of tables to determine the amount of tax.

The simplicity of this method explains why it is used almost universally. Payroll Deductions Tables contain withholding tables for weekly, biweekly, semi-monthly, and monthly deductions. Sections of the tables for persons paid weekly are illustrated in Below The steps in determining the amount to be withheld are:

- Choose the proper table based on the pay period.

- Find the line in the table that covers the amount of wages the employee earned.

- Follow across this line until you reach the column corresponding to the federal and

- provincial claim code. The amount shown at this point in the table is the income tax to be withheld.

- For example, Phillipe Castello is single, his in federal claim code 2 - with taxable earnings of $785, and provincial is B and his taxable earnings is $804.31 for the week. In the section of the table for persons paid weekly, appropriate line is the one covering wages between the range $779 to $787, his tax deduction is $51.20. In the Quebec tax table, on this line under the column headed "B," the Quebec tax is $66.28

The amount of federal and provincial income taxes to be withheld from the wages of each hourly employee of Marcof’s Furniture is determined in a similar manner from the sections of the weekly wage-bracket withholding tables shown here.

SAMPLE FEDERAL & PROVINICAL TAX TABLES

Federal Tax Weekly Deduction - Page 3

|

Quebec Tax Weekly Deduction - Pages 3 & 4

|

OTHER DEDUCTIONS REQUIRED BY LAW

Provinces require that provincial income tax be withheld from earnings of employees. The procedures are similar to those already explained for income tax withholding. Of course, the appropriate provincial withholding tables or tax rates must be used.For the sake of simplicity, we will assume that no other deductions from the wages of the hourly employees of Marcof’s Furniture are required by law.

In the case of Marcof’s Furniture, the only recurring "other deduction" is a deduction from an employee's pay for a part of the cost of health and hospitalization insurance for dependants of employees if employees choose to have dependants covered.

Marcof’s pays all health and hospitalization insurance premiums on each employee. In addition, it pays most of the premiums for coverage of the employee's spouse and dependants. However, the employee is required to pay a total of $18 per week for coverage of his or her spouse and other dependants.

In the case of Marcof’s Furniture, the only recurring "other deduction" is a deduction from an employee's pay for a part of the cost of health and hospitalization insurance for dependants of employees if employees choose to have dependants covered.

Marcof’s pays all health and hospitalization insurance premiums on each employee. In addition, it pays most of the premiums for coverage of the employee's spouse and dependants. However, the employee is required to pay a total of $18 per week for coverage of his or her spouse and other dependants.

QPP PENSION PLAN

Determine Employee Deductions for QPP Contributions

The QPP is levied in an equal amount on both the employer and the employee. The QPP contribution rate of 6.40 percent is applied to a base consisting of the first $63,100 of wages paid to an employee during the calendar year after the $3,500 basic personal exemption has been subtracted. Earnings in excess of the base amount are not taxed. If an employee works for more than one employer during the year, QPP contribution is deducted and matched by each employer.

When the employee files a provincial income tax return, any excess tax withheld from the employee's earnings is refunded by the government or applied to payment of the employee's provincial income taxes. The employer receives no refund merely because an employee held more than one job during the year.

The amount of QPP to be deducted can be computed either by multiplying the taxable wages by the QPP rate or by referring to tax tables found in Payroll Deductions Tables, published by and available from Ministère du Revenu du Québec.

When the employee files a provincial income tax return, any excess tax withheld from the employee's earnings is refunded by the government or applied to payment of the employee's provincial income taxes. The employer receives no refund merely because an employee held more than one job during the year.

The amount of QPP to be deducted can be computed either by multiplying the taxable wages by the QPP rate or by referring to tax tables found in Payroll Deductions Tables, published by and available from Ministère du Revenu du Québec.

SAMPLE QPP WEEKLY DEDUCTION TABLE

|

|

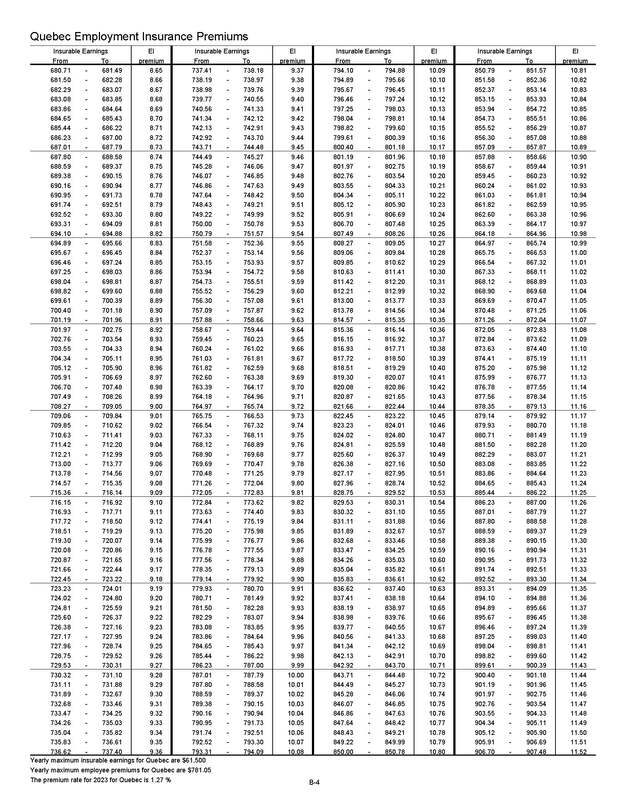

EMPLOYMENT INSURANCE PREMIUMS

Selecting the employee deductions for EI premiums

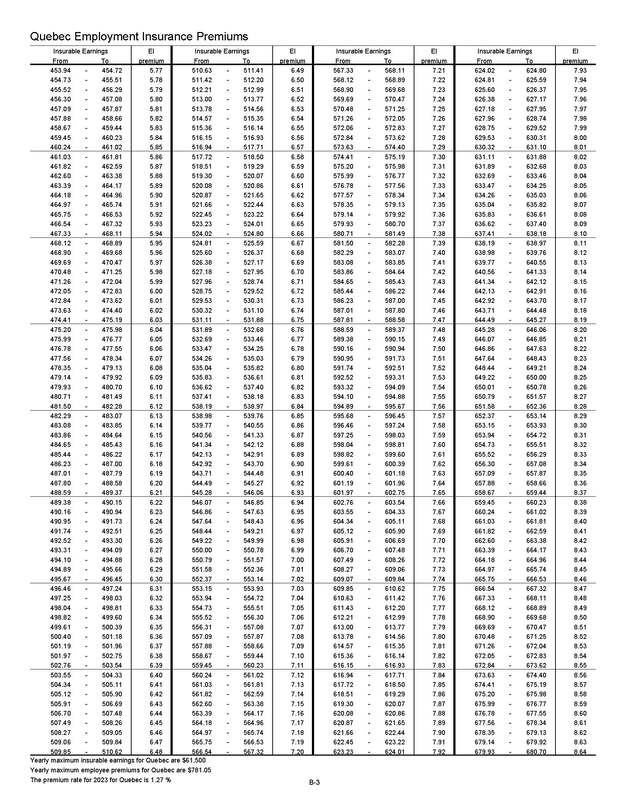

Employment insurance is levied on the employee and the employer. An EI rate of 1.27 percent employment insurance to a maximum of $61,500 is applied to all employees' salaries and wages.

While a worker is employed, a portion of the earnings is paid into an unemployment insurance fund. These premiums are deducted by an employer each pay period. Once the maximum is reached no more premiums are deducted. The amount to withhold for the employee is found in the tables.

While a worker is employed, a portion of the earnings is paid into an unemployment insurance fund. These premiums are deducted by an employer each pay period. Once the maximum is reached no more premiums are deducted. The amount to withhold for the employee is found in the tables.

Sample EI Deductions Table

|

|

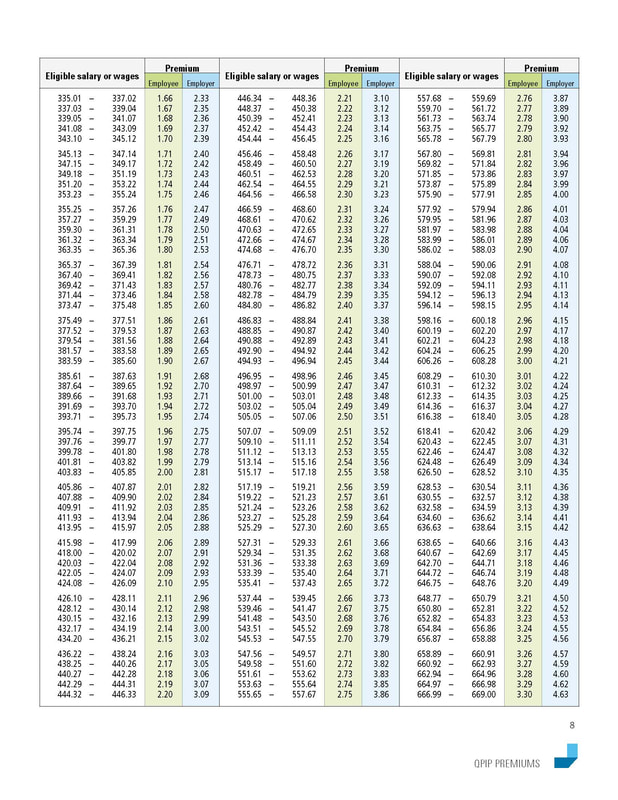

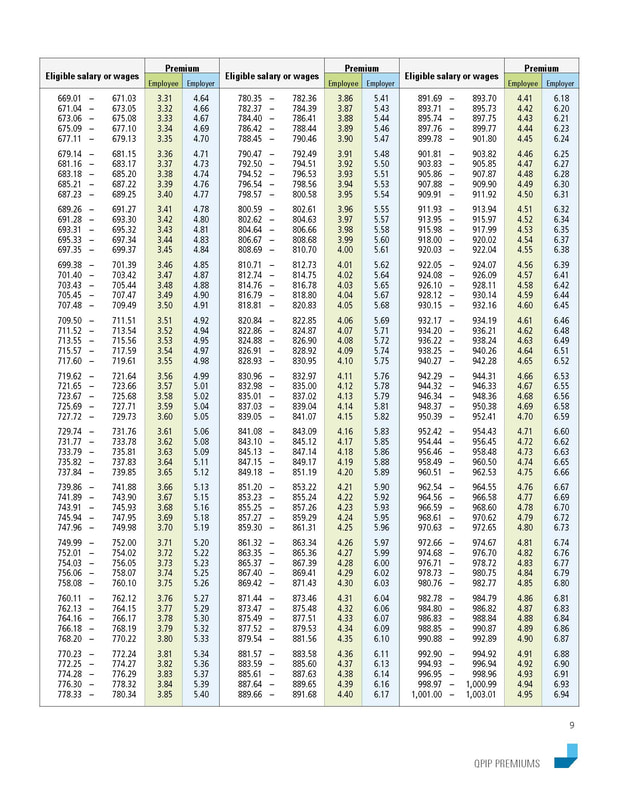

QUEBEC PARENTAL INSURANCE PLAN

All employees irrespective of their age and working in Canada must contribute to the QPIP. Payment of QPIP benefits are made to an employee who takes a maternity, paternity, adoption or parental leaving during which he or she sustains an interruption of earnings.

Regardless of the method of paying employees, QPIP contributions are deducted at end of each payroll period until the base amount of earnings for the calendar year is reached. The amounts to withhold for employees can be found in the deduction tables. Once the maximum contribution is reached no more premiums are deducted. This means, that the employer has to stop deducting premiums when the employee reaches the maximum 2023 deduction of $449.54.

Once a month, the company remits all deductions to the government. It must be emphasized that an employer must deduct QPIP premiums from all employees regardless of age.

Regardless of the method of paying employees, QPIP contributions are deducted at end of each payroll period until the base amount of earnings for the calendar year is reached. The amounts to withhold for employees can be found in the deduction tables. Once the maximum contribution is reached no more premiums are deducted. This means, that the employer has to stop deducting premiums when the employee reaches the maximum 2023 deduction of $449.54.

Once a month, the company remits all deductions to the government. It must be emphasized that an employer must deduct QPIP premiums from all employees regardless of age.

Sample QPIP Deductions Table

|

|

|

|

|